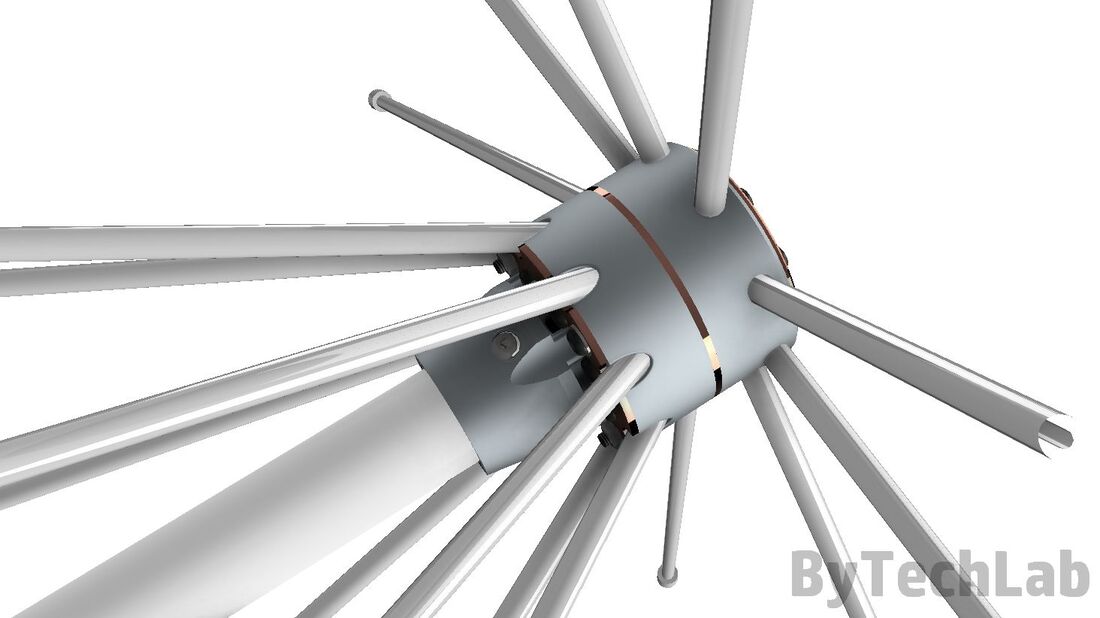

3D Printed Antenna Market Market Overview:

Global 3d Printed Antenna Market are electrical components used for transmission and reception of radio frequency signals. These antennas can be customized and manufactured in unique shapes and sizes which provides significant advantage over conventional antennas. Miniaturized antennas 3D printed with conductive materials allow convenient installation into devices and provide connectivity solutions across sectors. Market key trends: The emergence of miniaturization of antennas using 3D printing technologies is fueling market growth. Traditional antennas occupy significant space and are difficult to install in compact devices. 3D printed antennas are developed by optimizing antenna geometry and utilizing additive manufacturing which has allowed miniaturization up to 90% compared to traditional designs. The ability to manufacture customized miniature antennas in unique shapes and sizes using 3D printing is finding increasing demand for applications such as radio frequency identification, wearables, Internet of Things devices and more. This has driven research and development activities amongst market players to commercialize 3D printing of miniaturized antennas. Porter’s Analysis Threat of new entrants: New companies find it difficult to enter this niche market and gain market share as it requires significant R&D investments and established supply chains. Bargaining power of buyers: Individual buyers have low bargaining power due to the specialized nature of 3D printed antennas. However, large telecommunication companies wield significant influence. Bargaining power of suppliers: A few key material suppliers exist with specialized photopolymers and conductors used, allowing them to influence prices. Threat of new substitutes: No close substitutes exist currently for 3D printed antennas given their customized designs and mechanical properties. Competitive rivalry: Intense as key players compete on technology patents, product customization, and strategic partnerships. SWOT Analysis Strengths: Customized designs, lightweight properties, integration into IoT devices. Weaknesses: High production costs, limited sizes, and shapes. Supply chain issues. Opportunities: Growth of 5G networks, autonomous vehicles, telemedicine. Expanding into aerospace and defense. Threats: Strategic partnerships reducing barriers. Stringent regulatory approvals. Technology obsolescence risks. Key Takeaways The global 3D Printed Antenna market is expected to witness high growth, exhibiting CAGR of 16% over the forecast period, due to increasing demand for customized wireless solutions across industries. The market is estimated to reach US$ 1.7 billion in 2023. Regionally, North America dominates currently due to extensive research investments and 5G infrastructure projects. The Asia Pacific region is expected to be the fastest growing market, growing at a CAGR of over 18%, due to the expanding electronics and telecommunication industries in China and India. Key players operating in the 3D Printed Antenna market are Optisys LLC, Optomec Inc., Stratasys Ltd., Nano Dimension Ltd., Voxel8, Optomec Inc., Hanson Robotics, CRP Technology, The ExOne Company, Materialise NV, EOS GmbH, SABIC, HP Inc., GE Additive, Markforged. These players are focusing on new product launches, partnerships and mergers to gain leading market share. Read More: https://www.pressreleasebulletin.com/3d-printed-antenna-market-share-and-growth

0 Comments

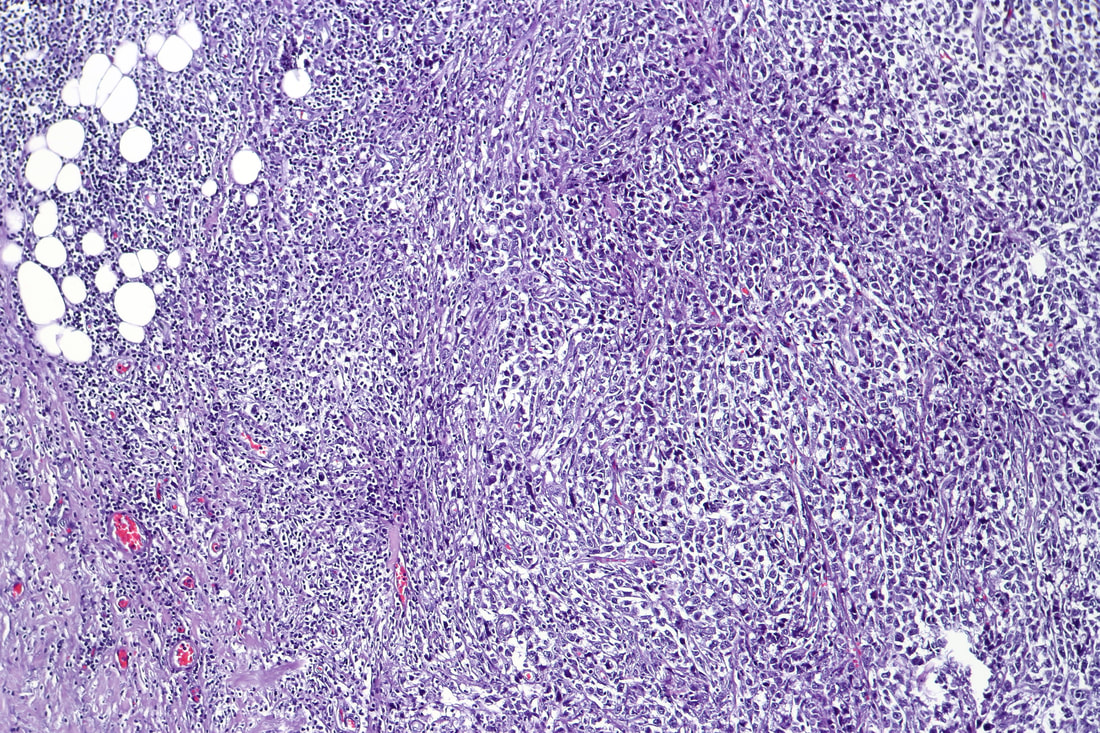

Relapsed Or Refractory Diffuse Large B Cell Lymphoma Market Market Overview:

Diffuse large B-cell lymphoma (DLBCL) is the most common subtype of non-Hodgkin lymphoma. It is an aggressive (fast-growing) form of cancer affecting B lymphocytes. Relapsed or refractory diffuse large B-cell lymphoma (R/R DLBCL) refers to lymphoma that returns after initial treatment or does not respond to first-line treatment. Current treatment options for R/R DLBCL include chemotherapy, immunotherapy, and stem cell transplantation. Targeted therapies such as monoclonal antibodies, antibody-drug conjugates, and CAR T-cell therapy have shown promising efficacy in treating R/R DLBCL in clinical trials. Market Dynamics: The Relapsed Or Refractory Diffuse Large B Cell Lymphoma Market is primarily driven by increasing incidence of R/R DLBCL worldwide. According to the Lymphoma Research Foundation, about 40% of people diagnosed with DLBCL will relapse at some point or become refractory to initial treatment. Furthermore, targeted therapies such as chimeric antigen receptor (CAR) T-cell therapy have gained regulatory approval in recent years for treating R/R DLBCL, which is driving their adoption. For instance, Segment Analysis The global relapsed or refractory diffuse large B cell lymphoma market is dominated by monotherapy as a treatment segment. This segment held around 60% market share in 2023 owing to favourable reimbursement policies and availability of generic versions of chemotherapy drugs used for monotherapy. PEST Analysis Political: The market is positively impacted by favourable government policies and regulations to boost adoption of innovative lymphoma treatment options. Economic: Rising healthcare spending global on oncology indication augurs well for market growth. Social: Growing awareness about lymphoma subtypes and available treatment options is driving patients to seek advanced relapsed/refractory diffuse large B cell lymphoma therapies. Technological: Rapid development of target therapies and immuno-oncology drugs with novel mechanisms of action are expanding treatment landscape for patients failing first-line therapy. Key Takeaways The global relapsed or refractory diffuse large B cell lymphoma market is expected to witness high growth, exhibiting CAGR of 4.3% over the forecast period, due to increasing adoption of combination therapies and pipeline drugs. The North America region is expected to dominate the market over the forecast period, owing to availability of advanced treatment options, robust research infrastructure, and favourable reimbursement policies in the region. Key players operating in the relapsed or refractory diffuse large B cell lymphoma market are MorphoSys U.S. Inc., Bristol-Myers Squibb Company, Karyopharm Therapeutics, Hoffmann-La Roche AG, Merck & Co., Inc., Gilead Sciences, Inc., Novartis AG, Regeneron Pharmaceuticals, Cellular Biomedicine Group Inc., Genmab A/S, Incyte, AbbVie Inc., Janssen Biotech, Inc., Pfizer Inc., IMV Inc., Overland Pharmaceuticals (CY) Inc., ADC Therapeutics SA, Eagle Pharmaceuticals, Inc., and Adaptive Biotechnologies Corporation. Read More: https://www.marketwebjournal.com/relapsed-or-refractory-diffuse-large-b-cell-lymphoma-market-trends/ Global Polyunsaturated Fatty Acids Market Is Estimated To Be Valued At US$ 5.89 Bn In 202310/31/2023  Polyunsaturated Fatty Acids Market Market Overview:

Polyunsaturated fatty acids are essential fatty acids that human body requires but does not produce on its own. These fatty acids help in lowering cholesterol levels, reducing blood pressure, managing weight, and reducing inflammation in the body. There are two major types of polyunsaturated fatty acids i.e. omega-3 and omega-6. Foods rich in omega-3 and omega-6 fatty acids include flaxseeds, chia seeds, walnuts, fatty fish etc. Increasing consumer awareness regarding health benefits of consuming adequate polyunsaturated fats is driving the growth of this market. Market key trends: Growing demand for fortified and functional food and beverages-: There is a rise in demand for functional and fortified food products over the past few years. Food manufacturers are focusing on fortifying various food products with polyunsaturated fatty acids to cater to this demand. For instance, companies offer milk, yogurt, cereal, flour etc. fortified with omega-3 fatty acids. This trend is expected to continue during the forecast period thereby propelling the market growth. Porter’s Analysis Threat of new entrants: The threat of new entrants is low as the Polyunsaturated Fatty Acids market requires high capital investment for R&D and production. Well established brands have economies of scale. Bargaining power of buyers: The bargaining power of buyers is high given the availability of substitutes. Buyers can easily shift to alternative sources to meet their requirements. Bargaining power of suppliers: A few major companies dominate the raw material supply chain giving them significant influence on price and availability of raw materials. Threat of new substitutes: New substitute products constantly enter the market posing a moderate threat. Manufacturers rely on innovation to cater niche segments. Competitive rivalry: Intense competition exists among the key players to expand market share through product differentiation, price points and strategic mergers. Key Takeaways The global Polyunsaturated Fatty Acids market Demand is expected to witness high growth, exhibiting CAGR of 8.2% over the forecast period, due to increasing health awareness and demand for nutritional supplements. Regional analysis: North America dominates the global Polyunsaturated Fatty Acids market followed by Europe and Asia Pacific. The Asia Pacific region is expected to witness fastest growth due increased disposable income, growing middle class and their focus on quality diet. Key players operating in the Polyunsaturated Fatty Acids market are Koninklijke DSM N.V, BASF SE, Croda International PLC, Enzymotec Ltd., Omega Protein Corporation, Aker Bio Marine AS, Polaris Nutritional Lipids, FMC Corporation, Cargill, Incorporated, GlaxoSmithKline plc. Key players are focused on new product launches, partnerships and capacity expansion strategies to strengthen their market presence. Read More: https://www.dailyprbulletin.com/polyunsaturated-fatty-acids-market-demand-and-growth/  India power tools Market Market Overview:

Power tools are power-operated devices that are used to perform different construction, woodworking, metalworking, and other tasks faster than manually operated tools. Power tools include drills, saws, sanders, grinders, routers, and others. These tools are widely used in construction, woodworking, and metalworking industries in India. Market Dynamics: The India power tools market is expected to witness significant growth, owing to increasing construction activity in the country. Rapid urbanization and industrialization have boosted residential and commercial construction activities across various cities in India. This increase in construction projects is expected to propel the demand for power tools during the forecast period. In addition, the presence of several established players such as Bosch, Stanley Black & Decker, and Makita Corporation are continuously introducing advanced and innovative power tool solutions in the Indian market, which is further expected to support market growth over the forecast period. SWOT Analysis Strength: Power tools market in India holds great potential with respect to commercial and industrial construction. Presence of ample skilled labor force specialized in construction activities provides competitive advantage. Availability of raw materials domestically helps reduce dependency on imports. Large population base with growing demand for infrastructure and real estate development supports market growth. Weakness: Unorganized small players dominate Indian power tools market. Lack of investment in R&D limits product innovation. Fluctuating raw material prices pose challenge. Increased penetration of imported and counterfeit products threatens domestic manufacturers. Opportunity: Rising ‘Made in India’ initiative and favorable governmental policies attract global power tools brands. Growing need for technological advancement in agriculture and manufacturing sectors opens new avenues. Rising per capita income and changing lifestyles fuel do-it-yourself (DIY) trend among individuals. Threats: Stiff competition from established international brands pressures pricing and supply chain management. Volatile economic conditions and downturn in key end-use industries weaken demand growth. Stringent environmental and safety regulations increase compliance costs. Key Takeaways The global India India Power Tools Market Share is expected to witness high growth, exhibiting CAGR of 8.9% over the forecast period, due to increasing infrastructural development and industrialization. The market was valued at US$ 802.1 Mn in 2022. Regional analysis The western region dominates India power tools market with over 35% market share in 2022 owing to highest infrastructure development activities in states like Maharashtra and Gujarat. The southern region is anticipated to grow at fastest pace during forecast period backed by large-scale investment planned for smart cities and urbanization projects. Key players Key players operating in the India power tools market are Apex Tool Group LLC, Atlas Copco AB, Emerson Electric, Co Techtronic Industries, Hilti Corporation, Stanley Black & Decker, Ingersoll-Rand plc, Robert Bosch, Koki Holdings Co., Ltd., and Makita Corporation. Techtronic Industries led the market with over 20% revenue share in 2022. Read More: https://www.marketwebjournal.com/india-power-tools-market-to-grow/  Market Overview:

The clinical diagnostic market involves providing solutions that aid in the diagnosis of diseases through various clinical tests on patient samples such as blood, urine, tissue biopsies, and others. These diagnostic solutions include instruments, reagents, and software that assist physicians in accurate diagnosis to determine the appropriate treatment. With the growing disease burden and need for early diagnosis, the demand for advanced clinical diagnostic solutions is increasing globally. Market Dynamics: The growth of the clinical diagnostic market is driven by the growing adoption of advanced diagnostic technologies among medical professionals owing to their benefits such as improved accuracy, fast results, and high throughput of testing samples. Furthermore, continuous technological advancements in clinical diagnostic solutions such as automation, software integration, machine learning-enabled diagnostics are further fueling the market growth. The increasing investments by key players to develop innovative solutions as well as growing demand from emerging economies with large patient pools are likely to present lucrative opportunities over the forecast period. Segment Analysis The Clinical Diagnostic Market Demand is segmented into immunochemistry, clinical microbiology, point of care testing, hematology, and tissue diagnostics. The immunochemistry segment dominates the market and accounted for over 25% share in 2021. This is because immunochemistry assays help detect diseases by identifying proteins produced in response to infections or other pathogens. They provide accurate, objective, and faster results compared to conventional procedures. PEST Analysis Political: Regulations supporting disease diagnosis and monitoring positively impact the market. However, uncertain reimbursement policies can hamper market growth. Economic: Rising per capita healthcare spends, growing middle-class incomes in developing nations drive market expansion. Social: Aging population and increasing incidence of chronic and infectious diseases propel diagnostic test demands. Technological: Adoption of automation, digitization, and AI techniques enhances testing efficiency and quality. Miniaturization leads to point-of-care testing devices. Key Takeaways The global clinical diagnostic market is expected to witness high growth, exhibiting CAGR of 6.1% over the forecast period, due to increasing disease incidence, rising elderly population, and growing awareness. Regional analysis: North America dominated with over 35% share in 2021 led by the US owing to rapid adoption of advanced technologies, presence of leading players, and well-established healthcare infrastructure. Asia Pacific is expected to be the fastest-growing region owing to large patient pool, increasing healthcare investments, and growing medical tourism in India and China. Key players operating in the clinical diagnostic market are Thermo Fisher Scientific, F. Hoffmann-La Roche AG, Qiagen N.V, Hologic Inc., Siemens Healthineers AG, BioMerieux SA, Abbott Laboratories, Bio-Rad Laboratories Inc., Becton, Dickinson and Company, and Danaher Corporation (Beckman Coulter, Inc.), among others. Read More: https://www.marketwebjournal.com/clinical-diagnostic-market-demand-growth-and-share/  Train Seat Materials Market Market Overview:

Train seat materials are crucial components used in train carriages for providing comfort and safety to passengers. Various foam, fabric and leather materials are widely used for manufacturing train seats. Appropriate train seat materials help in absorbing impact and vibration during travel while ensuring long-term durability. Market key trends: The growth of the global train seat materials market is primarily driven by the increasing focus of railway operators and authorities on providing enhanced passenger comfort and safety. Various material innovations are being adopted to develop breathable, durable and lightweight train seat covers along with temperature responsive cushions and foams. Foam padding materials infused with gel or copper fibers are gaining traction as they help in dissipating heat and reducing pressure points. Rising adoption of automated manufacturing processes by key players is also supporting the large scale production of customized train seat components. Furthermore, stringent regulations regarding fire-retardant properties of materials used in public transport are promoting the demand for engineered plastics and hybrid fabrics. Train Seat Materials Market Demand are utilized in manufacturing train seats for enhanced comfort and durability. Various materials are used including fabrics, foams, and composites depending upon the requirements. Majorly used materials include fabrics made from wool, cotton, polyester, and leather for upholstering train seats. Foams including polyurethane, silicone, and memory foams are incorporated underneath the fabric covers for providing cushioning and comfort. Composites consisting of hybrid materials and reinforced plastics are also emerging as sustainable options. Market Dynamics: Rising passenger traffic on trains across regions is driving the demand for additional coach capacity and replacement of old fleets, thereby propelling the train seat materials market growth. According to the International Union of Railways, the number of passenger journeys on trains reached over 5 billion in 2021, reflecting a rise of 21% as compared to 2020. Furthermore, material manufacturers are focusing on developing sustainable and lightweight materials for train seats through innovations. Adoption of composite materials incorporated with recyclable plastics and natural fibers is gaining traction in the industry. Additionally, memory foams offering enhanced circulation and ergonomic designs are being increasingly preferred. Such developments are expected to boost the train seat materials market during the forecast period. Key players operating in the train seat materials market are Rescroft Ltd., USSC Group, Inc., Magna International, Inc., Rojac Urethane Limited, GRAMMER AG, TransCal, Freedman Seating Co., Delimajaya Group, Franz Kiel GmbH, iFoam Ltd., Compin-Fainsa, FlexoFoam Pvt. Ltd., FISA Srl, FENIX Group, LLC, and Kustom Seating Unlimited, Inc. and Others. Major players are focusing on developing novel, lightweight and eco-friendly train seat materials to strengthen their market position. Read More: https://www.marketwebjournal.com/the-train-seat-materials-market-growing-demand/  Market Overview:

Industrial energy efficiency market comprises products and services that help to reduce industrial energy consumption while maintaining the same or improved level of output. These include products such as LED lighting, conveyor belt systems, industrial boilers and heat exchangers. Increasing focus on reducing energy costs and carbon emissions from industrial facilities is driving demand for industrial energy efficiency solutions. Market key trends: One of the key trend spurring growth of the Industrial Energy Efficiency Market Share is the rapid emergence of new technologies for renewable energy integration. Renewable energy technologies such as solar PV and wind are being increasingly deployed at industrial facilities to generate on-site power. Advancements in energy storage solutions are also enabling greater utilization of renewable energy by industries. This is expected to significantly reduce dependence on grid power as well as fossil fuels, driving demand for technologically advanced industrial energy efficiency solutions in the coming years. Porter’s Analysis Threat of new entrants: Low capital requirements and existing technologies act as a barrier for new players. Moreover, presence of established brands makes it difficult for new entrants to gain market share. Bargaining power of buyers: Large buyers can negotiate for better prices and customized solutions due to their high purchase volumes. However, availability of several solution providers counterbalances their bargaining power. Bargaining power of suppliers: Majority of components and equipment required can be easily sourced from different suppliers. This limits the bargaining power of suppliers. Threat of new substitutes: Emerging technologies like IoT provide an opportunity for alternate solutions. However, established application areas and customer acceptance favors existing products. Competitive rivalry: The market consists of global giants with overlapping product portfolios. Players differentiate based on product innovation, service quality and geographic penetration to gain competitive edge. SWOT Analysis Strengths: Growing investments and policy push for resource efficiency. Vast application areas across industries and availability of advanced technologies. Weaknesses: High initial costs deter certain customer segments. Complex implementation and dependency on external expertise. Opportunities: Rising energy consumption, carbon emission regulations and automation & digitization trends. Growth prospects in emerging markets. Threats: Economic slowdowns impacting capital expenditure budgets. Protectionist trade policies affecting global collaborations and supply chain. Key Takeaways The global industrial energy efficiency market size is expected to witness high growth, exhibiting CAGR of 8.6% over the forecast period, due to increasing focus on carbon emission cuts and sustainable development goals. Power generation, cement, chemicals and food & beverage industries cumulatively account for over 45% share of global energy consumption, thereby, driving large-scale deployment of energy management solutions. Regional analysis - North America currently holds the largest share in the market supported by stringent environmental regulations and rapid industrialization. Asia Pacific is poised to emerge as the fastest growing regional market by 2030 on account of rising manufacturing activities, urbanization and government programs promoting energy conservation in major countries like China and India. Key players - Key players operating in the industrial energy efficiency market are Siemens, General Electric, ABB, Johnson Controls, Schneider Electric, Honeywell, Eaton Corporation, Rockwell Automation, Emerson Electric, Mitsubishi Electric, Yokogawa Electric. They provide integrated solutions ranging from plant automation & control systems to renewable energy integration, facility management and engineering services. Read More: https://www.dailyprbulletin.com/industrial-energy-efficiency-market-demand-size-and-share/  Market Overview:

Buy now pay later platforms have enabled consumers to purchase goods and pay for them later through easy monthly instalments rather than paying the full amount upfront. These platforms provide a more affordable and flexible payment option especially for big-ticket items. They have proliferated e-commerce sales by providing customers the means to better manage cash flows and budget expenses. The model benefits both consumers and merchants. Market Dynamics: The Mena And Cis buy now pay later platform market is projected for robust growth owing to rising e-commerce sales in the region and initiatives to increase financial inclusion across developing nations. According to the United Nations Conference on Trade and Development, e-commerce sales in the Middle East and North Africa reached $26 billion in 2019 indicating immense untapped potential. Additionally, as per Economist Intelligence Unit, credit card penetration in the Middle East is amongst the lowest globally at 10%. Buy now pay later schemes help address the credit gap by offering convenient credit lines to more consumers. They empower customers with responsible spending power and flexibility to pay later over time which further fuels retail spending especially for luxury items. The payment flexibility coupled with increasing internet usage on mobile devices is anticipated to significantly contribute to the regional BNPL market growth over the forecast period. Segment Analysis The Mena And Cis Buy Now Pay Later Platform Market can be segmented into the service type and application. Based on service type, deferred payment dominates the segment as it enables customers to pay for purchases in interest-free installments over a period of time. Consumers prefer deferred payment as it allows flexible repayment options without charging late fees. PEST Analysis Political: The regulations around the BNPL industry in MENA and CIS region are evolving. Some countries have introduced stricter rules around late payment fees and credit checks to protect consumers. Economic: The rising internet and smartphone penetration along with growing e-commerce industry is propelling the adoption of BNPL platforms in the region. The young population is driving consumption. Social: Changing consumer preferences towards instant purchases and online shopping are increasing the popularity of BNPL services. Consumers find it convenient to split payments for purchases. Technological: Advancements in payment gateway technologies are making digital payment options more secure and convenient. Emergence of open banking is allowing BNPL providers to integrate with banks seamlessly. Key Takeaways The Mena And Cis Buy Now Pay Later Platform market size was valued at US$ 1152.6 Mn in 2021 and is expected to witness high growth, exhibiting a CAGR of 8.2% over the forecast period. The growth is attributed to the increasing adoption of digital payment modes and rising online shopping among consumers in the region. Geographically, the MENA region dominated the market in 2021 due to the booming e-commerce industry and high smartphone penetration in countries like Saudi Arabia and UAE. However, CIS countries are expected to be the fastest growing segment owing to the expansion of leading BNPL players and developing digital payment infrastructure in Russia. Key players operating in the Mena And Cis Buy Now Pay Later Platform are Afterpay, Holdings Inc., Klarna Bank AB, Laybuy Group Holdings Limited, Payl8r (Social Money Ltd.), PayPal Holdings Inc., Perpay, Quadpay. All the major BNPL providers are focusing on strategic partnerships and collaborations with local banks and merchants to expand their share in the high potential region. Read More: https://www.marketwebjournal.com/mena-and-cis-buy-now-pay-later-platform-market-growth/  China Continuous Glucose Monitoring Devices Market Market Overview:

Continuous glucose monitoring devices help people with diabetes to measure glucose levels in real time without painful fingersticks. The devices work by measuring glucose levels in interstitial fluid via a small sensor that is usually inserted underneath the skin. This provides timely data on trends and patterns to help diabetes patients make effective treatment decisions. Market key trends: One of the major trends driving the China continuous glucose monitoring devices market is the incorporation of augmented reality and virtual reality capabilities. Emerging CGM devices are being integrated with AR/VR technologies to provide enhanced visualization of glucose data. This allows patients to view trends and patterns overlaid on a virtual interface for improved understanding. Furthermore, AI capabilities are enabling personalized alerts and notifications based on individual patterns as detected by CGM sensors. The integration of advanced technologies thus helps drive better diabetes management outcomes through customized care approaches. Porter’s Analysis Threat of new entrants: The threat of new entrants is moderate as the development of continuous glucose monitoring devices requires huge research and development investments. Bargaining power of buyers: The bargaining power of buyers is high since there are many players operating in the market providing substitutable products to consumers. Bargaining power of suppliers: The bargaining power of suppliers is moderate as raw material suppliers have limited influence over the prices owing to availability of substitute raw materials. Threat of new substitutes: The threat of new substitutes is moderate due to requirements of regulatory approvals and certifications. Competitive rivalry: High. SWOT Analysis Strength: The China Continuous Glucose Monitoring Devices Market has high growth potential due to increasing incidence of diabetes. Weakness: Minimal reimbursement for CGM devices limits their adoption. High cost of innovative products is another weakness. Opportunity: Growing geriatric population susceptible to diabetes offers opportunities for market players. Rising awareness about benefits of CGMs presents an opportunity. Threats: Stringent regulatory framework and longer timelines for approval poses a threat. Reimbursement policies remain a challenge. Key Takeaways The global China Continuous Glucose Monitoring Devices market is expected to witness high growth, exhibiting CAGR of 22.8% over the forecast period, due to increasing incidence of diabetes. The market size is projected to reach US$ 176.4 million by 2023. Regional analysis: China dominates the CGM devices market in the region with more than 50% market share due to large patient pool and government support. Other rapidly growing markets include Japan and South Korea. Key players operating in the China Continuous Glucose Monitoring Devices market are Medtronic PLC, Abbott Laboratories, Medtrum Technologies, Inc., Senseonics, Nemaura, STMicroelectronics, NXP Semiconductors, Qualcomm, Taiwan Semiconductor Manufacturing Company Limited, GE Healthcare, Microchip Technology Inc., Texas Instruments Inc., Micron Technology Inc., Renesas Electronics Corporation, and Toshiba Corporation. Read More: https://www.marketwebjournal.com/china-continuous-glucose-monitoring-devices-market-growth  Track and Trace Solutions Market Market Overview:

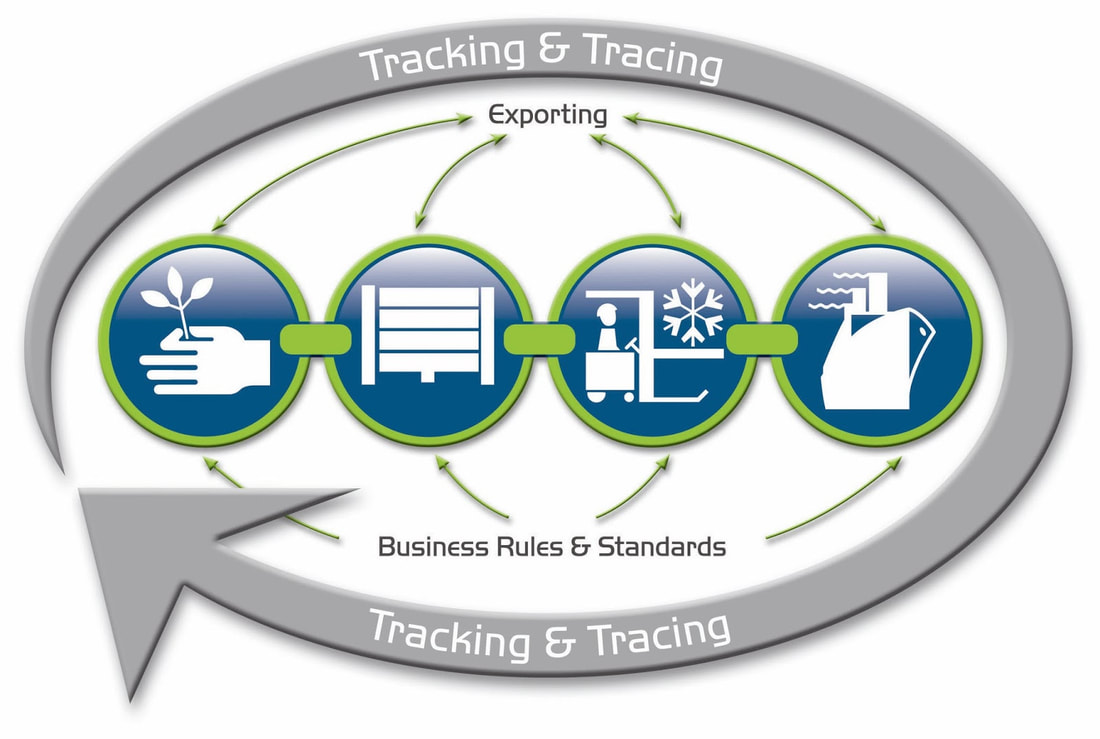

Track and trace solutions enable serialization, and aggregation of pharmaceutical products at packaging levels. It helps in validating authentic products and identifying counterfeit ones. The solutions ensure product safety and security across distributors and supply chain by providing visibility and traceability of goods. Market key trends: One of the major trends driving the market growth is the stringent regulations imposed by regulatory bodies across countries regarding implementation of track and trace solutions. For instance, the U.S. Drug Supply Chain Security Act (DSCSA) mandates serialization and traceability of pharmaceutical products. Similarly, the European Falsified Medicines Directive includes compliance to serialization deadlines. This is boosting adoption of track and trace solutions among pharmaceutical manufacturers and supply chain stakeholders to ensure product authenticity right from production to patient level. The solutions enable scanning of unique identification codes at different points to track product movement and history in supply chain. This enhances supply chain efficiency and security. Porter’s Analysis Threat of new entrants: Low capital requirements and online distribution channels have lowered entry barriers. However, established companies have significant brand loyalty and economies of scale. Bargaining power of buyers: Large buyers have significant influence due to their purchase volumes but track and trace is mandatory for compliance so choice is limited. Bargaining power of suppliers: A few large innovative suppliers exist but many smaller suppliers provide substitutes. Suppliers have moderate power due to differentiated products. Threat of new substitutes: Track and trace is mandatory for certain industries so substitution threat is low. However, emerging technologies may disrupt current solutions. Competitive rivalry: Intense as major players compete on pricing, innovation and integration with other supply chain solutions. Acquisitions are common to expand capabilities. SWOT Analysis Strengths: Track And Trace Solutions Market Demand ensures supply chain compliance and visibility. Digitalization offers real-time data exchange and analytics. Weaknesses: Initial costs and change management requirements. Operational complexities of legacy systems integration. Opportunities: Expanding regulations andSerialization requirements present growth avenues. Integration within larger digital supply chain initiatives. Threats: Stricter privacy laws may limit data usage. Lower cost alternatives or disruptive technologies from newcomers. Key Takeaways The global track and trace solutions market is expected to witness high growth, exhibiting CAGR of 14.79% over the forecast period, due to increasing regulatory mandates for supply chain transparency and safety. North America dominated the market in 2022 with a share of over 35%, due to stringent regulations and established pharma and biotech industry in the region. Asia Pacific is anticipated to be the fastest growing region due to expanding generic drug manufacturing in India and China along with growing focus on brand protection. Key players operating in the track and trace solutions market are Tracelink Inc., Adents International, Seidenader Maschinenbau Gmbh., Axway Software Sa, Siemens Ag, Mettler Toledo International Inc., Robert Bosch Gmbh, and Optel Group. Tracelink Inc. and Axway Software Sa hold a significant share due to their early mover advantage and continue investing in enhancing serialization and aggregation solutions. Emerging players are also focusing on multi-client national encoding platforms. Read More: https://www.marketwebjournal.com/track-and-trace-solutions-market-growth/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2024

Categories |

RSS Feed

RSS Feed