Commercial Drones Market The commercial drones market comprises aerial robots and associated services used majorly for applications ranging from infrastructure inspection, agriculture monitoring, product delivery and more. Powered by lithium-polymer batteries, commercial drones are equipped with cameras, thermal sensors and other tools to capture images. Their compact size enables inspection of areas impossible to reach through manual methods safely. The growth in e-commerce and quick delivery demands has boosted their use for logistics. Furthermore, they aid in monitoring agricultural fields, surveying construction sites and inspecting infrastructure like power lines, pipelines and cellular towers at a lower cost compared to manned aircraft.

The Global Commercial Drones Market is estimated to be valued at US$ 22.29 Bn in 2024 and is expected to exhibit a CAGR of 13% over the forecast period 2024 to 2031. The demand for Global Commercial Drones Market Growth is increasing across sectors like construction, e-commerce, agriculture and government. Reconstruction and infrastructure projects across developing nations are majorly driving their deployment for monitoring, surveying and inspection activities. Additionally, advancements in precision agriculture have propelled their adoption for crop health assessment, soil and field mapping. Key Takeaways Key players operating in the commercial drones market are Lockheed Martin Corporation, Northrop Grumman., The Boeing Company, BAE Systems PLC, Airbus S.A.S., FLIR Systems, Inc., Aero Vironment, Inc., Textron Inc., Aeryon Labs Inc., General Atomics, Thales, Quantum Systems, Elistair, Delair, DJI and Ehang. The growing application of commercial drones for various industrial uses such as infrastructure monitoring, agriculture surveillance, product delivery and inspection has fueled the market growth. Furthermore, technological advancements including integration of thermal sensors, quantum systems and beyond line of sight capabilities have augmented their capabilities. Technological innovations are further strengthening the capabilities of commercial drones. Beyond line of sight operations, quantum-assisted sensing and thermal imaging are enhancing surveillance and inspection accuracy. Miniaturization of components and increased battery life has led to the development of compact multi-rotor drones. In addition, AI & ML innovations are empowering commercial drones with autonomous flight, obstacle detection and analytics capabilities. Market Trends Rise of drone fleets - With increasing scope of applications, vendors are focusing on development of centralized control systems for commercial drone fleets. This enables remote monitoring and coordinated operations across multiple drones. Advancements in battery technologies - Lithium sulfur and lithium air batteries with higher energy density compared to existing lithium-ion variants are being developed. This will increase flight time of commercial drones. Growth of drone logistics - Firms are testing drones for delivery of medical supplies, packages and food items. Technological advancements will boost their commercial integration into logistics by the end of the decade. Market Opportunities Infrastructure inspection - Emerging economies provide major opportunities for commercial drones to automate inspection of utilities, cell towers, pipelines, roads and railways. Precision agriculture - Their scope for supporting and enhancing agricultural operations across crop analysis, irrigation and monitoring will continue growing. Disaster management - Drones can play a bigger role in rescue operations, assessing damage from floods, earthquakes and assessing wildfires. Their portfolio in emergency response will expand. Impact of COVID-19 on Commercial Drones Market The COVID-19 pandemic significantly impacted the commercial drones market growth globally. The lockdowns imposed worldwide led to disruptions in manufacturing and supply chains. This restricted the production of drones and their components which declined the market growth initially in 2020. However, with easing of restrictions from mid-2021, the market started recovering gradually. During the pandemic, drones were extensively used for delivery of essential goods like food, medicines etc. and for monitoring social distancing in public places. They proved helpful for authorities and organizations to function efficiently without risking human lives. This boosted the demand for commercial drones during the crisis and is likely to fuel their increased adoption post-pandemic for ensuring safety, improving operations and enabling contactless delivery services. However, factors like reduced discretionary spending and delayed capital expenditure plans of enterprises impacted the overall market. With economies stabilizing and normalization of operations, the commercial drones market is expected to gain strong momentum in coming years. Geographical Regions with Highest Commercial Drones Market Value North America accounted for the largest share of the global commercial drones market in terms of value in 2024. This is attributed to high adoption of commercial drones across various industries like agriculture, infrastructure, energy & resources and public sector in countries like United States and Canada. Significant government investments to develop advanced drone technologies and presence of major market players in the region have propelled the market growth. Asia Pacific is expected to be the fastest growing regional market between 2024-2031 driven by increasing applications of drones in industries like construction, agriculture and e-commerce coupled with favorable government regulations in countries like China, India and South Korea. Fastest Growing Geographical Region for Commercial Drones Market Asia Pacific is projected to be the fastest growing region for the commercial drones market during the forecast period of 2024-2031. This is attributed to rapid urbanization, rising construction activities and expanding e-commerce industry in the region. Countries like China, India, Japan, South Korea and Australia are showing increased acceptance and deployment of commercial drones for various applications. The agriculture sector in Asia Pacific nations is adopting drones for crop monitoring, soil and field analysis which is fueling the market growth. Favorable government initiatives to leverage drone technologies and rising investments by market players have augmented the regional market expansion. Thus, Asia Pacific offers lucrative opportunities for commercial drones with expected double digit growth rate during the next 7 years. Get more insights on this topic: Commercial Drones Market

0 Comments

Global Automotive Fastener Market The global automotive fastener market consists of various fastening components such as screws, nuts, bolts, washers, and rivets that are used to join automotive vehicle parts and components by mechanical fastening method. Automotive fasteners are made from various materials such as stainless steel, carbon steel, aluminum, nickel, etc. to provide optimal performance in different temperatures and weather conditions. Fasteners are crucial for assembling an automotive as they hold critical components like engines, chassis, wheels, and other structural parts together. They not only join vehicle parts but also provide strength and protection against vibration. With rise in automotive production around the world due to increasing vehicle ownership, demand for various fastening components is growing steadily.

The Global Automotive Fastener Market is estimated to be valued at US$ 33.9 Bn in 2024 and is expected to exhibit a CAGR of 4.7% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Global Automotive Fastener Market Share are Atotech Deutschland GmbH, Birmingham Fastener, Inc., Bulten AB, Jiangsu Xing Chang Jiang International Co., Ltd., KAMAX, KOVA Fasteners Private Limited, Lisi Group, PennEngineering, Permanent Technologies, Inc., Phillips screw company, SFS Group, Shamrock International Fasteners, Shanghai Prime Machinery Company, Shanghai Tianbao Fastener Manufacturing Co., Ltd., Stanley Black & Decker, Sundram Fasteners Limited, Westfield Fasteners Limited. The automotive fastener market is experiencing high demand due to increased automotive production across the world. According to projections, the global vehicle production is estimated to rise from 95 million units in 2020 to 118 million units by 2025. This increase in automotive manufacturing activities will necessitate more fastening components in vehicles. Advanced technologies such as 3D printing are being utilized to manufacture light weight and durable fasteners with complex geometries for automotive applications. Additive manufacturing allows designing fasteners conforming to precise industry standards with ease. Market Trends Increase in Electric Vehicles (EVs) - Many automakers are heavily investing in electric vehicles to comply with stringent emission norms. This will elevate the demand for fasteners optimized for EV batteries and powertrains. Advent of Lightweight Fasteners - Weight reduction is a key focus area for automakers to boost fuel efficiency. Lightweight fasteners made of composite materials and 3D printing techniques are gaining traction. Market Opportunities Growth in Aftermarket Sales - Regular replacement and maintenance of fasteners in old vehicles presents opportunities for aftermarket businesses. Collaborations with Automotive OEMs - Fastener manufacturers can directly collaborate with vehicle brands for design validation and newer product developments. This will strengthen supply chain relations. Impact of COVID-19 on Global Automotive Fastener Market The outbreak of COVID-19 pandemic has impacted the growth of global automotive fastener market negatively in 2020. The lockdowns imposed by various governments globally led to shutdown of automotive production facilities. This resulted in decline in demand for automotive fasteners from OEMs. The supply chain was disrupted significantly causing shortage of raw materials for automotive fastener manufacturers. However, the demand is expected to recover post pandemic as the automotive production resumes with ease in lockdown restrictions. The automotive fastener market players need to focus on establishing robust supply chain network and maintain inventory to cater future demand. Diversifying supplier base can help manufacturers mitigate future supply risks. Adopting innovative manufacturing technologies can help improve productivity and meet future demand efficiently. Geographical Regions with High Concentration in Global Automotive Fastener Market In terms of value, Asia Pacific region accounts for the largest share in global automotive fastener market owing to presence of major automotive hubs like China, Japan and India. China dominates the APAC automotive fastener market with largest vehicle production in the world. North America and Europe are other major regions concentrated for automotive fastener market. The growing electric vehicle market and vehicle lightweighting trend is driving demand for innovative fastening solutions in these regions. Fastest Growing Region in Global Automotive Fastener Market The Middle East and Africa region is poised to emerge as the fastest growing region in global automotive fastener market during the forecast period. Countries like Saudi Arabia, South Africa, UAE are witnessing surge in vehicle production and sales which is propelling demand for automotive components including fasteners. Growing automotive aftermarket in Africa further supports the market growth. Moreover, investments by major automakers in developing manufacturing facilities in the region will substantially contribute to the fastest growth of automotive fastener market in Middle East and Africa over the coming years. Get more insights on this topic: Global Automotive Fastener Market  Cloud Native Software Market Cloud native software allows applications to leverage capabilities of modern clouds such as scalability, availability and elasticity at a lower cost without vendor lock-in. Cloud native software architectures rely on microservices that are independently deployable and provide a loosely coupled system that is highly scalable and agile. The rising adoption of DevOps methodologies and containers are fueling the adoption of cloud native technologies across organizations. Continuous delivery and automated deployments are increasingly being adopted which rely on cloud native architectures.

The Global Cloud Native Software Market Share is estimated to be valued at US$ 6.69 Bn in 2024 and is expected to exhibit a CAGR of 34.8 over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Cloud Native Software market are Boston Scientific, Merit Medical Systems,Cook Medical, Terumo Corporation, BTG Medical, Sirtex Medical, C.R. Bard. The increasing adoption of cloud-based technologies across enterprises is driving demand for cloud native software. Cloud native capabilities allow organizations to dynamically scale their applications up or down depending on computing requirements which is fueling adoption. Advancements in container technologies such as Docker and Kubernetes along with serverless computing are enhancing the potential of cloud native architecture by eliminating dependencies for manual resource management. Market Trends Microservices architecture is being adopted widely as it allows decomposition of monolithic applications into independently deployable services. This enhances scalability, flexibility and facilitates continuous delivery in cloud native applications. Serverless computing is gaining traction as it frees developers from the need to manage infrastructure and allows them to focus only on code. Serverless architectures are well-suited for event-driven applications and absorb computing fluctuations easily. Market Opportunities Growing demand from Small and Medium Enterprises for scalable and agile applications at low costs provides significant opportunities for cloud native software vendors. Leveraging artificial intelligence and machine learning capabilities of cloud platforms can enhance cloud native applications with advanced analytics capabilities. Integration of serverless capabilities with containers promises to optimize resource utilization further for cloud native deployments. Impact of COVID-19 on Cloud Native Software Market Growth The outbreak of COVID-19 pandemic has significantly impacted the growth of cloud native software market across the globe. The imposition of lockdowns and travel restrictions compelled many businesses and individuals to adopt work from home practices. This led to huge surge in demand for cloud-based collaboration tools, virtual private networks and other enterprise cloud solutions to ensure business continuity. Many cloud native software providers witnessed substantial increase in demand for their products and services as digitalization became imperative amid the pandemic. However, factors like supply chain disruptions and changing economic conditions posed certain challenges initially. With the progressive lifting of lockdowns and resumption of business activities, the demand is regaining momentum steadily. Many organizations have now realized the strategic importance of cloud infrastructure and are focusing on migrating more of their workloads and applications to public clouds. This is creating ample growth opportunities for specialized cloud native software vendors. Moreover, the pandemic has accelerated the digital transformation journeys of companies across industries. Emerging technologies like AI, IoT, blockchain are being increasingly adopted which is further fueling the adoption of microservices, containers and other cloud native architectures. Looking ahead, the cloud native software market is expected to grow at an even faster pace supported by ongoing technology modernization efforts of enterprises. Western Europe Region Concentrates Highest Value for Cloud Native Software Market The Western Europe region accounts for the largest share of the global cloud native software market in terms of value. Countries like Germany, UK, France have strong presence of leading cloud service providers as well as robust digital infrastructure. Enterprises across verticals in these countries have traditionally been early adopters of advanced technologies. Furthermore, factors like stringent data residency and compliance mandates are driving more organizations to leverage privately hosted clouds and cloud native applications. High spending capabilities and technology affinity of users in Western European countries also contribute to the high market concentration in the region. Asia Pacific Emerging as the Fastest Growing Region On the other hand, the Asia Pacific region is expected to witness the fastest growth in the cloud native software market over the forecast period. Proliferation of digital services and favourable government policies supporting technology deployments are fueling market expansion in Asia Pacific countries. Rapid infrastructure development, rising technology adoption among SMEs and startups along with growing consumer demand for digital services are some of the key factors accentuating the growth of cloud native software market in Asia Pacific region. Nations like China, India, South Korea, Australia, Singapore are at the forefront of this high growth trajectory. Get more insights on this topic: Cloud Native Software Market  Cyclocomputer Market Cyclocomputers are electronic devices that are mainly used to calculate and record cycling-related data such as speed, distance, time, and altitude. Features such as heart-rate monitoring, GPS route tracking, customizable workout programs, safety tracking, remote notifications, and wireless connectivity to smartphones have further increased their popularity. Rapid urbanization and growing health awareness have boosted participation in outdoor sports and fitness activities. Cyclocomputers help cyclists track their performance metrics and improve training programs. The global cyclocomputer market is estimated to be valued at US$ 625.43 billion in 2024 and is expected to exhibit a CAGR of 4.8% over the forecast period 2024 to 2031.

Key Takeaways Key players operating in the Global Cyclocomputer market Share include Morita Corporation, Alpha Dent Implants Ltd., Shofu Dental Corporation, Coltene Group, 3M Company, Institut Straumann AG, Zimmer Biomet, Dentsply Sirona Inc., DiaDent Group International, and Essential Dental Systems Inc., among others. Growing popularity of cycling as a fitness and recreational activity has boosted the demand for advanced cyclocomputers. Devices with integrated GPS, heart rate monitoring, and smartphone connectivity have gained widespread acceptance among amateur and professional cyclists. Technological advancements have enabled the development of feature-rich and affordable cyclocomputers. Touchscreen interfaces, ANT+ and Bluetooth connectivity, long battery life, and rugged and water-resistant designs are some of the trends observed in modern cyclocomputers. Market Trends Increased demand for rugged and waterproof cyclocomputers: Manufacturers are focusing on developing devices that can withstand challenging weather conditions like rain and dust. Waterproof and shockproof models suitable for mountain biking and adventure sports are gaining traction. Multi-sport compatibility: Consumers prefer devices that can record metrics for other outdoor activities like running, hiking, and swimming in addition to cycling. Features like compatible sensors are being integrated. Market Opportunities Scope for customized workout programs and algorithms: Working with fitness experts, companies can develop unique training regimens tailored to individual needs and improve route suggestions. growth of smart bikes and e-bikes: The rise of connected bikes provides opportunities to integrate advanced cyclocomputer features directly into bicycles. This could drive further adoption. How COVID-19 has impacted Cyclocomputer Market Growth The COVID-19 pandemic has had a major impact on the growth of the cyclocomputer market. During the initial lockdown phases across various regions, revenues declined significantly as the sales and production of cyclocomputers reduced substantially. People were advised to avoid outdoor activities and non-essential travel to curb the spread of the virus. This led to a steep decline in demand for cyclocomputers as bicycling became limited mainly to essential commuting. However, with increasing focus on health and fitness even during the pandemic, bicycling saw a renewed interest as an outdoor recreational activity preferred by many to maintain physical and mental well-being during lockdowns. As restrictions eased in later months, the demand for cyclocomputers started recovering. Many people took to cycling as a way to exercise and commute while maintaining social distancing. This boosted the sales of entry-level cyclocomputers. However, the high-end professional models witnessed relatively slower recovery. Supply chain disruptions also presented challenges initially but the market is expected to normalize post-pandemic with continuing interest in cycling supported activities. Overall, while COVID-19 slowed down growth temporarily, increased focus on health and outdoors is likely to support the long-term prospects of this market. Europe remains the largest geographic market for Cyclocomputers Europe currently dominates the global cyclocomputer market in terms of value, accounting for over 35% share. Countries like Germany, France, Italy, UK and others have seen significant demand over the years led by presence of major manufacturers, developed cycling infrastructure and culture, rising health awareness as well as large amateur racing communities. However, the Asia Pacific region is emerging as the fastest growing regional market. Countries like China, Japan and India are witnessing fastest adoption led by growing middle class, increasing emphasis on preventive healthcare through activities like cycling, development of domestic manufacturing base and infrastructure expansion supporting cycling as environment friendly mobility option. The APAC region is expected to surpass Europe in terms of overall sales volume in the coming years though Europe will continue leading in terms of value of high-end professional cyclocomputers. Get more insights on this topic: Cyclocomputer Market  Alprazolam Tablets Market The Alprazolam tablets market consists of oral tablets that contain alprazolam as the active pharmaceutical ingredient. Alprazolam is a benzodiazepine derivative and acts as an agonist of the gamma-aminobutyric acid (GABA) receptor in the central nervous system. It is primarily used as an anxiolytic and panic disorder treatment to reduce anxiety and induce calmness. Alprazolam tablets help reduce physical symptoms associated with anxiety and panic attacks like rapid heartbeat, sweating, trembling, and chest pain. The growing prevalence of anxiety disorders caused due to stress, mental illness, and unhealthy lifestyles is a major driver for the alprazolam tablets market. In addition, the rising elderly population prone to anxiety problems also fuels market growth.

The Global Alprazolam Tablets Market Demand is estimated to be valued at US$ 3243.65 Mn in 2024 and is expected to exhibit a CAGR of 8.0% over the forecast period 2024 To 2031. Key Takeaways Key players operating in the Alprazolam tablets market are Haesung Optics Co. Ltd., Largan Precision Co. Ltd., Tamron Co. Ltd., Sunny Optical Technology (Group) Company Limited, Sunex Inc., Kantatsu Co. Ltd., Ability opto-Electronics Technology Co. Ltd., Genius Electronic Optical Co. Ltd., AAC Technologies Holdings Inc., SEKONIX Co. Ltd., and IM Co. Ltd. Major pharmaceutical companies are focusing on introducing generic versions of alprazolam tablets to gain more market share. The growing prevalence of anxiety and panic disorders worldwide is fueling the demand for alprazolam tablets. Technological advancements in drug delivery systems aim to reduce dosing frequency and improve medication adherence through controlled-release formulations. Market Trends One of the key trends in the alprazolam tablets market is the growing preference for generic drugs. The patent expiration of branded alprazolam tablets has led to a surge in low-cost generic alternatives. This has substantially lowered treatment costs and improved patient accessibility. Another trend is the rising demand for controlled-release and extended-release formulations. These advanced drug delivery systems help achieve steady blood concentrations of the drug for an extended period with fewer dosage intakes. This enhances patient compliance and treatment effectiveness. Market Opportunities One of the major opportunities for players in the alprazolam tablets market is to expand into untapped emerging economies. Countries in Latin America, Asia Pacific, Africa, and Eastern Europe have high unmet needs for anxiety treatment due to lack of mental healthcare infrastructure and access to medications. There is room for greater market penetration through favorable regulatory policies and investments. Another opportunity lies in developing novel delivery mechanisms like sublingual and buccal films. These routes of administration provide a fast therapeutic effect while bypassing first-pass metabolism for improved bioavailability. Impact of COVID-19 on Alprazolam Tablets Market Growth The outbreak of COVID-19 has significantly impacted the growth of the alprazolam tablets market as people are being advised to avoid non-essential hospital visits during this crisis. However, the demand for alprazolam tablets used to treat anxiety and panic disorder increased among COVID-19 patients to manage stress and mental health issues. This led pharmaceutical companies to ramp up production to meet this surge in demand. The fear and uncertainty around the pandemic also triggered anxiety and panic among the general public which further boosted sales of alprazolam tablets. However, nationwide lockdowns imposed restrictions on the mobility of goods which disrupted manufacturing and supply chains initially. This caused a temporary shortage of alprazolam tablets in the market. With easing of lockdown measures, production and distribution channels were restored, normalizing the availability of tablets. Pharmaceutical companies also adopted various preventive measures in manufacturing facilities like social distancing, improved sanitization and use of protective equipment.This helped in continuation of alprazolam tablet production during the crisis. Moving forward, the market is expected to grow steadily as mental health issues have become an area of increased focus due to long term anxiety caused by the pandemic. Companies will need to strengthen supply chains and inventory management to ensure efficient availability of the tablets in the market. Investments in advanced online platforms for doctor consultations and home delivery of medicines can further aid the market's growth in the post-COVID phase. Geographical Regions with Highest Alprazolam Tablets Market Value North America dominated the global alprazolam tablets market in terms of value owing to a high prevalence of anxiety disorders and greater health awareness. Large pharmaceutical companies with strong branded and generic portfolios also operate from the US and Canada fueling market revenues. Asia Pacific has emerged as the fastest growing regional market for alprazolam tablets driven by a surge in stress disorders among a growing middle class population coupled with increasing medical access. Rising income levels have also augmented healthcare spending on neuropsychiatric medications like alprazolam tablets in developing countries like India and China. Additionally, growing pharmaceutical sectors and relocation of manufacturing bases to these low-cost regions will continue supporting the market's expansion. Get more insights on this topic: Alprazolam Tablets Market  Atomic Force Microscope Market An atomic force microscope (AFM) is a type of scanning probe microscope with demonstrated resolution on the order of fractions of a nanometer, enough to show individual atoms. AFMs help characterize material properties on the nanoscale, reveal details of processes such as formation of deposits or corrosion and provide ways to measure small forces between surfaces. The need for high-resolution and high-precision surface imaging in various industrial applications has boosted the demand for atomic force microscopes globally.

The Global Atomic Force Microscope Market Share is estimated to be valued at US$ 602.4 Mn in 2024 and is expected to exhibit a CAGR of 4.8% over the forecast period from 2024 to 2031. Key Takeaways Key players operating in the atomic force microscope market are Bruker, Semilab Inc., Oxford Instruments, Anton Paar, Attocube Systems AG, Novascan Technologies, Inc., Nanosurf AG, Nanonics Imaging Ltd, Nanomagnetics Instruments, NT-MDT Spectrum Instruments and Advanced Technologies Center. The growing manufacturing sector along with increasing need for precision and quality control has booted AFM demand. Technological advancements have made AFM systems more affordable for routine applications in industry and academic settings. Market Trends Increasing applications in material science: Atomic force microscopes are increasingly used for material characterization tasks like studying thin film structures, quantifying mechanical properties and surface chemistry analysis. They are valuable research tools in academia and industry R&D for semiconductor and materials development. Growing adoption in industrial quality control: AFMs are used for failure analysis, defect detection and nanomanufacturing quality control tasks. Their high resolution makes them suitable for precision applications in sectors like electronics, energy and automotive for tasks like studying tribology, catalysts and printed circuits. This is a major growth driver for atomic force microscopes. Market Opportunities Life sciences and healthcare applications: AFM is valuable for cell biology, protein structure analysis and high-resolution imaging in pharmaceutical R&D. Growing healthcare expenditures and need for precision diagnostic tools will drive its demand. Integration with other techniques: Combined techniques like AFM-Raman and AFM-FTIR are seeing increased adoption as they provide comprehensive chemical and physical analysis. This integrated approach is an opportunity to develop advanced product variants. Impact of COVID-19 on Atomic Force Microscope Market The COVID-19 pandemic negatively impacted the growth of the atomic force microscope market in 2020. During the initial months of lockdowns and social distancing restrictions imposed by governments worldwide, production and supply chain activities were disrupted. This led to reduced availability of atomic force microscope systems and their components. Several planned developments related to research institutes, universities and industries which involve utilization of atomic force microscope were postponed or delayed. However, with rising investments and focus on vaccine development and virus research, demand for atomic force microscope increased post-2020. Their high resolution imaging capability is leveraged for studying virus morphology, host cell interactions and effects of antiviral drugs. Market players responded with initiatives like remote access to atomic force microscope systems to enable continuity of research from home. New collaborations also emerged between industry and academia to accelerate COVID-19 associated projects utilizing atomic force microscope. Looking ahead, the pandemic has highlighted the criticality of atomic force microscopes in medical and life sciences sectors. There is increased government funding for infectious disease preparedness which will drive further procurement of advanced microscopy tools. Market participants need to strengthen production and supply chains to meet rising demand from vaccine/therapeutic development programs. Partnerships for upskilling researchers in atomic force microscope techniques can boost post-pandemic productivity and innovation. Geographical Regions with high Atomic Force Microscope market value North America accounted for the largest share of the global atomic force microscope market in terms of value in 2024. This was attributed to substantial investments by research universities and pharmaceutical companies in the US and Canada for nanotechnology and material science applications of atomic force microscope. presence of leading market players and availability of skilled workforce have reinforced the region's dominance. Europe was the second largest regional market driven by extensive funding from European Union towards advanced materials characterization, bioscience and healthcare technology development initiatives leveraging atomic force microscope capabilities. Countries such as Germany, UK and France have emerged as major domestic markets as well as export hubs. Fastest growing region for Atomic Force Microscope market Asia Pacific region is poised to register the fastest growth in the global atomic force microscope market during the forecast period of 2024 to 2031. This can be accredited to expanding research infrastructure in India and China coupled with rising private sector investments in semiconductor, energy and life science sectors. Initiatives promoting local manufacturing of analytical instruments will provide impetus. Additionally, technology transfers between more established markets and developing Asia Pacific economies will accelerate the region's growth trajectory. Get more insights on this topic: Atomic Force Microscope Market Live Package Tracking Market The live package tracking market enables customers to track the real-time location and delivery status of packages ordered online or via courier services. Live tracking provides enhanced visibility and control over package delivery. Customers can track packages through various touchpoints such as websites, mobile applications, SMS, and e-mail updates. This ensures quick delivery and instant notifications of package status. The growing demand for faster deliveries coupled with increasing cross-border e-commerce activities is propelling the live package tracking market. The global live package tracking market is estimated to be valued at US$ 4.52 Bn in 2024 and is expected to exhibit a CAGR of 9.2% over the forecast period 2024 to 2030.

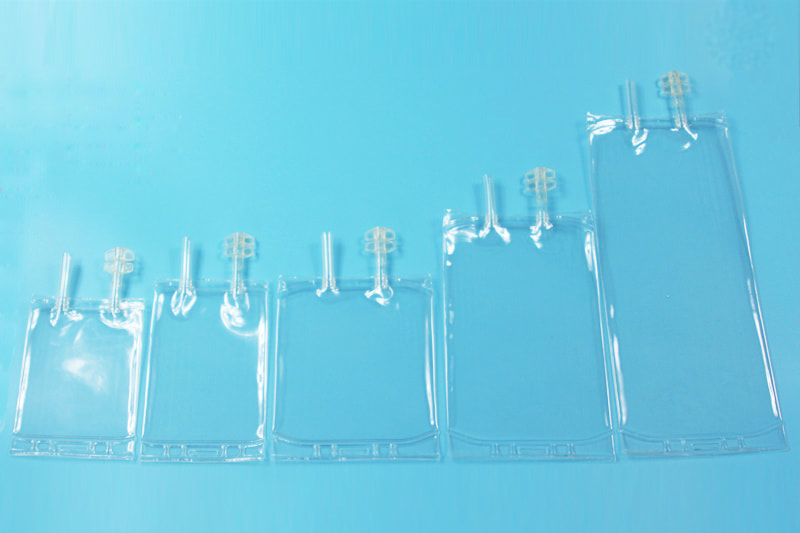

Key Takeaways Key players operating in the live package tracking market are Marriott International, Inc., Hilton Worldwide Holdings Inc., Accor S.A., InterContinental Hotels Group PLC, CWT (formerly Carlson Wagonlit Travel). Marriott International dominates the market with the largest hotel network worldwide. The growing e-commerce industry is fueling the demand for Global Live package tracking Market Demand solutions. Rapidly increasing online orders due to growing internet and smartphone penetration is prompting logistics companies to offer real-time package tracking to enhance customer satisfaction. Live tracking allows customers to plan their schedules according to package delivery times. Technological innovations are supporting the growth of live tracking. Advancements like IoT, RFID, AI, and machine learning are enabling logistics companies to track packages through multiple touchpoints and notify customers proactively. Analytics tools help optimize delivery routes and schedules. Blockchain technology is also being explored to securely track shipments in real-time across supply chains. Market Trends Customized tracking alerts : Vendors are offering customizable notification options through which users can choose delivery status updates to be received via medium of their preference like SMS, email, or mobile push. This ensures seamless visibility for customers. Multimodal transport tracking: Capability to track shipments across different transportation modes like air, road, and sea is a key trend. This gives end-to-end tracking across complex logistics networks. Market Opportunities Last mile delivery tracking: HighScopes for live tracking solutions focused on last mile deliveries to provide enhanced control and certainty for last mile deliveries reaching customers accurately. International shipment tracking: Cross-border logistics provides opportunities for live tracking solutions to securely monitor international shipments movements transparently. Clearance delays can be addressed proactively. Impact of COVID-19 on Live Package Tracking Market Growth The outbreak of COVID-19 pandemic has significantly impacted the growth of live package tracking market. During the initial phase of pandemic, majority of the countries announced nationwide lockdowns which disrupted the global supply chains and logistics operations. This led to delays in package deliveries and supply orders. Consequently, the demand for live package tracking solutions surged significantly as consumers wanted to track the real-time location of their packages. The live tracking helped in eliminating uncertainties around package deliveries which increased consumer trust in e-commerce. As the lockdowns eased across regions, the logistics operations resumed gradually. However, the demand for contactless deliveries continued to rise due to safety concerns. This further propelled the adoption of live package tracking solutions as they allowed receivers to receive packages without any physical contact. Additionally, the need to maintain social distancing norms encouraged logistics companies to optimize their operations and improve visibility with live package tracking. Going forward, the consumer preference for e-commerce is expected to remain strong even in post-COVID world which will augment the growth of live package tracking market. Europe currently contributes the largest market share for live package tracking globally. Countries like United Kingdom, Germany, France have well-established e-commerce markets with high package delivery volumes. The disruptions caused by COVID-19 pandemic further strengthened the market in the region. Asia Pacific is projected to be the fastest growing regional market during the forecast period. Countries like China, India witnessed massive surge in online shopping during pandemic. This is expected to fuel the demand for live package tracking solutions from logistics service providers and shipping companies operating across Asia Pacific in coming years. Get more insights on this topic: Live Package Tracking Market The Global Empty IV Bags Market will grow at highest pace owing to rising healthcare expenditure4/15/2024  Global Empty IV Bags Market The Global Empty IV Bags Market is a key component of the healthcare sector as it provides sterile storage and transportation solution for various drugs, pharmaceuticals, nutrients, and fluids. Empty IV bags are made from plastics such as PVC, Ethylene Vinyl Acetate (EVA), and polypropylene. Empty IV bags offer advantages such as avoiding cross-contamination, allowing flexible drug dosage, and providing protection against microbial infection. The rising demand for intravenous treatments among patients due to various chronic diseases and increasing number of surgical procedures are majorly driving the growth of the Empty IV Bags Market.

The Global Empty IV Bags Market is estimated to be valued at US$ 8.9 BN in 2024 and is expected to exhibit a CAGR of 9.0% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Global Empty IV Bags Market are POLYCINE GmbH, BAUSCH Advanced Technology Group, BD, Baxter, B. Braun Medical Inc., ICU MEDICAL, INC., Wipak, RENOLIT SE, TECHNOFLEX, Sippex IV bags, JW Life science Corp, and Fresenius Kabi AG. These players are focusing on new product launches and partnerships with pharmaceutical companies to expand their market presence. The rising prevalence of chronic diseases such as cancer, cardiovascular disorders, and inflammation is a major factor driving the demand for IV drug delivery globally. According to WHO, cardiovascular diseases account for over 17 million deaths annually worldwide. Nearly 70% of the global cancer burden is concentrated in Africa, Asia, and Central and South America. The increasing need to transport safe and sterile drugs for their treatment is propelling the Empty IV Bags Market. Technological advancements such as anti-reflex properties, contamination detection systems, and inclusion of tamper-evident seals in IV bags have improved product quality and safety. Manufacturers are increasingly developing customized empty IV bags suited for niche applications such as total parenteral nutrition and chemotherapy. This is expanding the potential of IV drug delivery and positively impacting the market. Market Trends Tailor-made IV bags - Manufacturers are focusing on developing customized empty IV bags suited for niche applications such as total parenteral nutrition, blood transfusion, chemotherapy, and antibiotics. This allows easy administration of specific drugs. Sustainable production - With rising environmental concerns, players are increasingly adopting sustainability practices such as utilizing recyclable plastics and reducing carbon footprint in bag production. This is expected to drive the demand for eco-friendly empty IV bags. Market Opportunities Emerging economies - Markets in developing regions such as Asia Pacific, Latin America, and Middle East are projected to generate highest growth opportunities owing to large patient pools and improving healthcare spending. Orphan drugs market - Growing popularity of orphan drugs for rare diseases offers significant potential for specialized empty IV bags tailored for orphan drug delivery. This presents an attractive avenue. Impact of COVID-19 on Empty IV Bags Market Growth The COVID-19 pandemic has significantly impacted the growth of the global empty IV bags market. During the initial months of the outbreak, the market experienced a decline in demand as most elective surgeries and non-essential medical procedures were postponed to avoid risk of infection. Hospitals focused on expanding their intensive care capacity and stocking up essential medical supplies to treat rising COVID-19 cases. However, as the pandemic became prolonged, the usage of IV bags increased significantly for treatment of coronavirus infected patients. IV therapy plays a vital role in hydration and medication administration for critically ill COVID-19 patients. This boosted demand for empty IV bags from 2020 onwards. With rising vaccination rates, the deferral of medical procedures is gradually being lifted which is further propelling market growth. However, ongoing supply chain disruptions continue to pose challenges. In the coming years, steady recovery in non-COVID healthcare and emphasis on stockpiling reserves is expected to drive sustained momentum. Geographical Regions with High Concentration of Empty IV Bags Market In terms of value, North America accounted for the major share of the global empty IV bags market and is expected to continue its dominance through the forecast period. This is attributed to factors such as rising prevalence of chronic diseases, growing geriatric population susceptible to health issues, high per capita healthcare expenditure, and accessibility to advanced medical technologies. Within the region, the US dominated other countries due to presence of well-established healthcare infrastructure and affiliates, and favorable reimbursement policies supporting usage of IV therapy products. Europe holds the second largest market share owing to increasing usage of IV therapy solutions in treatment of cancer, diabetes and other long-term conditions. Fastest Growing Regional Market for Empty IV Bags Asia Pacific is projected to witness the fastest growth in the empty IV bags market during the predicted years. This is due to improving access to advanced medical services across developing nations, rising healthcare investments, increasing demand for branded pharmaceuticals, and expanding patient pool of chronic diseases. Additionally, growing medical tourism industry attracting patients from Western nations seeking low-cost treatment options further aids growth. With presence of emerging economies experiencing high economic development such as China and India, the demand for IV bags is witnessing a constant surge in the Asia Pacific region. Get more insights on this topic: Global Empty IV Bags Market The Global Acute Dystonia Market will grow at highest pace owing to increasing R&D investments4/15/2024  Global Acute Dystonia Market Acute dystonia is a neurological movement disorder characterized by involuntary and sustained muscle contractions that result in abnormal repetitive movements or postures. It is commonly caused by medications such as drugs used to treat psychiatric conditions. The market is primarily driven by increasing prevalence of conditions causing acute dystonia such as Parkinson's disease, cerebral palsy and trauma. Anticholinergic drugs such as trihexyphenidyl hydrochloride are commonly used for the treatment of acute dystonia.

The Global Acute Dystonia Market is estimated to be valued at US$ 120.7 MN in 2024 and is expected to exhibit a CAGR of 3.2% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Global acute dystonia Market Growth are Fresenius Kabi, Amar Healthcare, Johnson & Johnson ,PAI Pharma, Pfizer Inc., Souvin Pharmaceuticals Pvt.Ltd, Bayer Healthcare, S.S.Pharmachem, Remedy Labs, Wan Bury, F. Hoffmann-La Roche Ltd, Bausch Health Companies, Inc., Viatris Inc. , Teva Pharmaceutical Industries Ltd, Torrent Pharmaceuticals Ltd., Mallinckrodt Pharmaceuticals, Amneal Pharmaceuticals LLC, Sun Pharmaceutical Industries Ltd., and Aurobindo Pharma Ltd. The increasing prevalence of neurological disorders and trauma cases is driving the demand for acute dystonia treatment. Major companies are focusing on developing novel drug delivery systems and new drug molecules to effectively treat acute dystonia. Market Trends Growing geriatric population: The risk of acute dystonia increases with age. As the geriatric population grows worldwide, the market is expected to witness lucrative opportunities owing to growing patient pool suffering from age-related neurological conditions. Increasing awareness: Initiatives by non-profit organizations and pharma companies to raise awareness about acute dystonia and its treatment options are helping more patients seek medical help. This is expected to positively influence the market growth. Market Opportunities Novel drug development: While anticholinergic drugs are commonly used, their effectiveness is limited in severe cases. There is scope for development of novel drugs with improved efficacy and safety profile to cater to unmet needs. Focus on emerging markets: Emerging countries in Asia Pacific and Latin America with large patient pools and growing healthcare spending present lucrative opportunities for both established and new market players. Penetration into these markets will be a key growth strategy. Impact of COVID-19 on Global Acute Dystonia Market Growth The COVID-19 pandemic has significantly impacted the growth of the global acute dystonia market. In the initial phases of the pandemic, dystonia treatments saw a sharp decline as outpatient facilities were shutdown and elective treatments were suspended to avoid virus spread and cater to rising COVID cases. This led to deferred treatments and diagnosis of dystonia, negatively impacting market revenue. However, with vaccination drives and relaxation of lockdowns, the market is regaining Lost momentum. Telehealth and online consultations have also picked up, enabling Continuity of care for dystonia patients. Nevertheless, the aftermath of the pandemic is expected to encourage faster market growth. With greater awareness about health issues, people are more inclined Towards managing chronic conditions proactively. This will drive higher dystonia diagnosis post-COVID. Moreover, drug developers are investing in novel therapies to overcome vaccine resistance and new variants of the virus. Such R&D investments may yield dystonia drugs with superior efficacy in the future. Healthcare providers are also better prepared Now to ensure uninterrupted services while following safety protocols. Overall, while COVID-19 dampened short term sales, the long term outlook for the global acute dystonia market remains positive with increased demand for advanced therapeutics. Geographical Regions with Major Market Concentration North America currently dominates the global acute dystonia market in terms of value, accounting for over 40% share. This is attributed to the high dystonia prevalence, strong healthcare infrastructure, and growing public awareness about movement disorders in the US and Canada. Moreover, leading global drug manufacturers are headquartered in the region, facilitating easy access to the latest treatment options. Asia Pacific is identified as the fastest growing market for acute dystonia globally. Factors such as the massive patient pool, rising healthcare expenditure, and improving diagnostic capabilities are fueling demand across developing countries like India and China. Several initiatives are being undertaken to make dystonia management more affordable and widespread in the region. This makes Asia Pacific an important investment hub for market players. Fastest Growing Region in Global Acute Dystonia Market Asia Pacific region holds immense growth potential for the acute dystonia market. Increased government focus on non-communicable diseases, growing private healthcare sector investment, and expansion of health insurance coverage are some key socio-economic changes augmenting market expansion. With prevalence of dystonia projected to surge over the next decade due to lifestyle changes and aging population, demand for medications from this region will spike. Market players are also strategizing distributor partnerships and generic production collaborations in Asia to tap the opportunities. Thus, backed by relentless economic growth, enhanced patient access, and rising medical standards, the acute dystonia market in Asia Pacific is well-positioned to witness double digit CAGR over the forecast period. Growing middle class population able to pay for premium drugs further strengthens the regions attractive prospects. Get more insights on this topic: Global Acute Dystonia Market  DNA test kits Market DNA test kits have gained immense popularity in recent years as they allow consumers to trace their family history and ancestry in a simple and accurate manner from the comfort of their homes. DNA test kits analyze saliva or cheek swab samples to determine genetic markers related to ethnicity estimates, physical traits, and health risks. The growing interest in self-exploration and scientific advancements that have made DNA testing more accessible and affordable is fueling massive demand for at-home genetic testing.

The Global DNA Test Kits Market is estimated to be valued at US$ 5.40 Bn in 2024 and is expected to exhibit a CAGR of 16% over the forecast period 2024 to 2031. Key players operating in the DNA Test Kits are Devyser, Illumina, Inc., Living DNA Ltd, MyHeritage Ltd., Gene by Gene, Ltd., Ancestry, EasyDNA, Fitness Genes, Living DNA Ltd., Helix OpCo LLC, Veritas, Genesis Healthcare Co., Mapmygenome, and Pathway Genomics. DNA test kits allow customers to gain valuable insight into their familial origins andinherited traits by analyzing specific genetic markers without visiting a clinical laboratory. The kits offer precise ethnicity estimates and relative relationships across global populations. advances in direct-to-consumer genetic testing have further simplified the process, generating accurate reports within weeks without requiring professional assistance. Key Takeaways Key players: Key players operating in the DNA Test Kits are Devyser, Illumina, Inc., Living DNA Ltd, MyHeritage Ltd., Gene by Gene, Ltd., Ancestry, EasyDNA, Fitness Genes, Living DNA Ltd., Helix OpCo LLC, Veritas, Genesis Healthcare Co., Mapmygenome, and Pathway Genomics. Growing demand: The popularity of at-home genetics services is being driven by factors like increasing consumer knowledge about genetic makeup and its role in personal health strategies, the potential to explore ancestral heritage, and availability of higher accuracy Global DNA Test Kits Market Share at affordable prices. Advancements in sequencing technologies and bioinformatics are also driving down costs. Technological advancement: Emergence of new Direct-to-Consumer ancestry and traits services; Companies are developing genetic analysis services for advanced traits like DNA-based diet and lifestyle suggestions. Introduction of technologies like whole genome sequencing would provide deeper insights into genetic predispositions. Market Trends Personalized Nutrition Recommendations - DNA test kits now provide consumers information on how their genes affect nutrition needs, metabolism, lifestyle habits like caffeine consumption and more. This empowers better dietary choices. Expanded Traits Analysis - Beyond ancestry, companies now analyze DNA for traits like earwax type, ability to taste bitterness in food, sleep patterns etc. for a more complete self-understanding. Market Opportunities Wellness Market Integration - DNA test results can be integrated into wellness programs, apps and services for a personalized holistic health experience. Non-Invasive Prenatal Testing Market - Fetal DNA analysis through maternal blood samples is gaining popularity. At-home tests analyse traits, parentage and genetic disorders. Impact of COVID-19 on DNA Test Kits Market The COVID-19 pandemic has significantly impacted the growth of the DNA test kits market. During the initial months of the pandemic, the market registered negative growth due to lockdowns and travel restrictions imposed by various governments. This led to supply chain disruptions and reduced demand as people were more focused on essential supplies. However, as lockdown restrictions eased in later months, the market started recovering. The demand for direct-to-consumer DNA test kits increased significantly during the pandemic as people spent more time at home and were interested in knowing their ancestry and health history. Restrictions on non-essential medical procedures pushed individuals to do at-home health and ancestry testing using DNA test kits. Several companies offered prominent discounts and offers during this period to boost sales. Going forward, the market is expected to grow at a faster pace in the post-COVID era. Companies are expanding their product portfolios to cater to rising demand. New tests for detecting genetic predisposition to diseases like Covid-19 are also being developed. Meanwhile, advanced kits for nutrition, fitness and pregnancy are gaining traction. With continued remote working and online classes becoming the new normal, online sales of DNA test kits will remain high. However, intermittent lockdowns and restrictions can act as challenges in some regions. Geography: Market Concentration in North America In terms of value, the DNA test kits market is highly concentrated in North America, primarily in the United States. This can be attributed to factors like growing awareness about DNA testing, established healthcare infrastructure to support genetic testing, easy availability of DTC kits and high per capita disposable incomes in the region. The region accounted for over 45% share of the global market in 2024, driven by high demand for ancestry, health and dog DNA test kits. Meanwhile, easy accessibility, engaged consumer bases and favourable regulations are supporting the market growth in the region. Fastest Growing Region: Asia Pacific The Asia Pacific region is expected to witness the fastest growth in the DNA test kits market during the forecast period. This can be attributed to rapidly growing healthcare infrastructure, rising awareness about genetic testing, increasing online penetration and burgeoning middle-class population with significant discretionary spending power in emerging countries like India and China. In addition, ongoing initiatives by governments as well as private entities to promote awareness regarding genetic testing and its benefits are supporting the regional market growth. Favourable policies implemented to encourage R&D activities in DNA sequencing and biomarkers are also boosting the Asia Pacific market. Moreover, growing penetration of international companies and expansion of DTC sites in the region will further aid the market expansion. Get more insights on this topic: Global DNA Test Kits Market |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2024

Categories

All

|

RSS Feed

RSS Feed