The castrate resistant prostate cancer market primarily comprises pharmaceutical drugs treating advanced stages of prostate cancer. These drugs offer palliative treatment for patients who have developed resistance against standard hormone therapies like surgical or chemical castration. Some of the common drug classes in this market include cytochrome P-450 17 inhibitor, androgen receptor antagonist, taxanes and several others. Rising prevalence of prostate cancer especially in developed nations is the key driver for widespread adoption of these advanced therapeutic drugs.

The Global Castrate Resistant Prostate Cancer Market Demand is estimated to be valued at US$ 12.82 Mn in 2024 and is expected to exhibit a CAGR of 6.6% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the castrate resistant prostate cancer market are Bucher Vaslin, Pera Pellenc, Scharfenberger, Zambelli Enotech, ENOTOOLS, Criveller Group, Della Toffola, Gruppo Bertolaso, Fabbri, Mori Luigi & C. The increasing incidence of prostate cancer worldwide has fueled the demand for advanced treatment options. As per statistics, around 1.3 million new cases of prostate cancer are reported annually globally. Moreover, the death rates associated with prostate cancer have also risen in the recent decades necessitating novel therapeutics. On the technological front, innovations in drug delivery mechanisms and development of novel drug molecules have expanded the treatment landscape for castrate resistant prostate cancer. Market trends Rising geriatric population susceptible to prostate cancer is a key trend propelling the castrate resistant prostate cancer market. Since the risk of prostate cancer rises sharply after the age of 65, developing nations with burgeoning shares of elderly are expected to significantly contribute to future market revenues. Another major trend is the increasing collaboration between drug makers to develop advanced therapeutic drugs through combinations and novel targets. This paves way for more efficacious drugs with better survival benefits. Market Opportunities An emerging opportunity is the development of personalized medicines tailored as per patient's genetic profile and tumor characteristics. This helps optimize treatment response rates. Secondly, immuno-oncology is an evolving area of opportunity with first-in-class immune modulators being tested for castrate resistant prostate cancer. Impact of COVID-19 on Castrate Resistant Prostate Cancer Market The COVID-19 pandemic has significantly impacted the growth of the castrate resistant prostate cancer market. During the initial outbreak and lockdowns imposed worldwide, access to healthcare facilities was limited. This resulted in postponed cancer treatments and surgeries. With postponed treatments, the demand and sales of drugs and therapies for castrate resistant prostate cancer reduced drastically in 2020. However, with rapid vaccination drives worldwide post-2021, healthcare facilities resumed full functioning with COVID protocols. This enabled cancer patients to restart their treatments. But the lingering effects of economic downturn due to the pandemic still continue to impact the market. Many patients have deferred or postponed their treatments due to financial constraints emerging from job losses or pay cuts during the pandemic. The drug development process was also delayed as clinical trials faced disruptions during lockdowns. pharma companies had to reallocate resources to COVID-19 vaccine and drug development. However, with economic recovery underway, the market is projected to bounce back to pre-pandemic growth levels by 2024. Pharma companies are expanding access to affordable therapies as well to overcome financial barriers emerging from the pandemic. The North American region accounts for the largest share of the global castrate resistant prostate cancer market in terms of value. This is attributed to factors such as rising geriatric population, increasing prevalence of prostate cancer, robust healthcare infrastructure and high healthcare spending in the US and Canada. The Asia Pacific region is projected to be the fastest growing regional market between 2024-2030. This is predominantly due to growing elderly demographics, improving healthcare access and rising healthcare spending in countries like China and India. The geographical region which concentrates highest value share for castrate resistant prostate cancer market is North America. This is because North America has the largest geriatric population suffering from prostate cancer along with highest per capita healthcare spending and availability of advanced treatment options. At the same time, Asia Pacific region is projected to grow fastest for castrate resistant prostate cancer market between 2024-2030. This is owing to rapidly aging population, rising healthcare access and fast economic growth leading to higher disposable income in countries like China and India. This enables more patients in Asia Pacific region to afford expensive castrate resistant prostate cancer drugs and therapies going forward. Get more insights on this topic: Castrate Resistant Prostate Cancer Marke

0 Comments

Shipbroking Market The shipbroking market involves services such as chartering, sale and purchase, and ship operations. These services help ship owners, cargo owners, traders, and other commercial maritime organizations in smooth operations and management of ships for transportation of goods via seas. Shipbroking plays an important role in facilitating international sea trade by bringing buyers and sellers together and negotiating deals on their behalf.

The Global shipbroking market Demand is estimated to be valued at US$ 289.53 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the shipbroking market are Doosan Heavy Industries & Construction,Toyota Turbine and Systems Inc.,Ballard Power Systems Inc.,Mitsubishi Electric Corp. ,Suzlon Energy Ltd.,Vestas Wind Systems A/S,Rolls-Royce Plc,Capstone Turbine Corp.,Sharp Corp.,General Electric. The shipbroking market offers opportunities for companies in sectors such as container shipping, dry bulk cargo, and crude and natural gas tankers owing to rapidly growing international sea trade. The increasing trend of globalization is also driving several organizations to outsource their shipping requirements to shipbrokers for seamless transportation of goods via international waters. Geographical expansion into emerging economies in Asia Pacific and Latin America through partnerships offer lucrative growth opportunities for shipbroking companies. Market drivers The key driver for the shipbroking market is the steady increase in international sea-borne trade volumes over the past few years. International organizations rely heavily on sea routes for import and export of commodities and goods. The shipbrokering services help organize shipping logistics for smooth transportation of cargo via sea. Their role in facilitating deals between shipping owners and cargo owners has become indispensable with growing trade volumes. This steady rise in global maritime trade supports the demand for specialized shipbroking services and drives growth of this market. PEST Analysis Political: The shipbroking industry is regulated by international maritime organizations and laws. Changes in trade policies, maritime regulations can impact shipbroking business. Economic: Global economic growth, international trade and seaborne trade volumes influence demand for ships and shipbroking services. Recession or trade wars can negatively impact shipping industry and shipbrokers. Social: Greater mobility and connectivity is increasing demand for transportation of goods via sea routes. Change in lifestyle and consumption patterns impact type of commodities shipped globally. Technological: Adoption of digital tools and blockchain for ship registration, tracking, documentation is streamlining processes. Automation, smart analytics help optimize routes and fleet deployment. Use of cleaner fuels is supporting green initiatives. The geographical region where the shipbroking market is concentrated in terms of value is Asia Pacific region. Asia Pacific accounts for over 35% of the global market value due to strong trade links within the region and with Europe and North America. China, Japan, South Korea are key trading nations driving significant ship movements and requirements of shipbroking intermediation services. The fastest growing region for the shipbroking market will be Latin America. With improving economic conditions and trade agreements, Latin American countries are increasing seaborne trade activities. Growing imports and exports of commodities from Latin America to Asia and Europe is bolstering trade volumes. This is slated to drive higher demand for shipping capacity and shipbroker assistance from Latin American ports during the forecast period. Get more insights on this topic: Shipbroking Market  Self-heating Food Packaging Market Self-heating food packaging involves use of integrated chemical reactors in packaging pouches and trays to heat up food products without any external heating source. These packaging solutions offer convenience of instantly heating foods such as meals, soups and beverages anywhere and anytime. Advantages of self-heating food packaging include portability, ease of use and safe and sterile heating without risk of burns. Rising consumption of convenience foods due to fast paced lifestyles has been a major driver for development and adoption of self-heating food packaging technologies.

The Global Self-heating Food Packaging Market is estimated to be valued at US$ 70.69 Mn in 2024 and is expected to exhibit a CAGR of 5.7% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the Global self-heating food packaging market Demand are Ceva, Zoetis, Elanco, Chanelle Pharma Group, and Boehringer Ingelheim International Gmbh, among others. Key players are focusing on developing advanced chemical reaction technologies for faster and controlled heating. They are also expanding their product portfolio catering to various food types. Growing demand for convenience and ready-to-eat food products is a major factor driving the self-heating food packaging market. Consumers preference for foods which can be eaten without preparation is increasing significantly. Self-heating packaging solutions fulfill the need for instant meals on the go. Technological advancements are expanding application areas of self-heating food packaging. Manufacturers are developing new chemical formulations for improved reaction control and compact package designs. Bio-based and recyclable chemical reactors are being researched to make these packaging solutions more sustainable. Intelligent packaging with temperature indicators and sensors is another emerging area. Market Trends - Microwavable self-heating food packages are a growing trend. They offer optionality of conventional microwave heating along with chemical heating. This increases convenience for consumers. - Development of flexible and portable packages for individual servings is gaining momentum. Products ranging from drink pouches to food envelopes are being designed for on-the-go consumption. Market Opportunities - Growing demand for healthy convenience foods provides opportunities for development of self-heating food packages for nutrition-rich products like soups and meals. - Emergence of self-catering trends due to remote working is boosting scope for customized and localized product offerings from manufacturers. Producing packs for regional cuisines can drive volumes. Impact of COVID-19 on Self-heating Food Packaging Market Growth The COVID-19 pandemic has adversely impacted the growth of the self-heating food packaging market. The lockdowns imposed globally disrupted the supply chains and halted production facilities. This led to a shortage of raw materials for manufacturing self-heating food packaging products. With people forced to stay indoors, the demand for ready-to-eat food items also saw a dip initially. However, as the restrictions have now eased in many regions, the market is demonstrating signs of recovery. Manufacturers are focusing on innovating their product offerings to align with the changing needs and habits of consumers. The increased preference for home-cooked and ready-to-eat meals is benefiting the market. Self-heating food packaging allows for convenient and safe consumption of food during the ongoing crisis. Companies are developing sustainable and affordable solutions to cater to the growing demand. Governments are also supporting local producers through initiatives that promote packaged food products. With rising health awareness, manufacturers will have to ensure stringent quality and hygiene standards. Adopting advanced technologies for contactless packaging and distribution will remain a key focus. Overall, while the pandemic imposed challenges, the self-heating food packaging market is well-positioned for steady growth in the coming years backed by innovations and evolving consumer lifestyles. The value of the self-heating food packaging market is concentrated majorly in regions like North America and Europe. The growing working population and busy schedules have increased the demand for ready meals and convenient food options in these developed markets. Easy availability of raw materials and sophisticated production facilities also contribute to the large market size of these regions. The Asia Pacific region is projected to be the fastest growing market for self-heating food packaging. With improving economic conditions and rising disposable incomes, people are willing to pay more for innovative packaged food products ensuring safety and hygiene. Countries like China, India and South East Asian nations offer immense scope for market expansion driven by rapid urbanization, westernization of diets and developing retail infrastructure. Government schemes to promote local manufacturing will further aid the market growth in Asia Pacific. For more insights, Read- Self-heating Food Packaging Market  Self-care Medical Devices Market The self-care medical devices market comprises products such as glucose meters, blood pressure monitors, pulse oximeters, pedometers, sleep apnea monitors, and neonatal devices. Self-care medical devices enable patients to monitor health vitals such as blood glucose, blood pressure, and body temperature at home and assist in effectively managing chronic diseases without physician intervention. The adoption of self-care medical devices help lower healthcare costs and reduce hospital visits.

The Global self-care medical devices Market is estimated to be valued at US$ 25.69 Bn in 2024 and is expected to exhibit a CAGR of 4.6% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the self-care medical devices market are Hans Zipperle AG, Archer Daniels Midland Company, Kerry Group. Growing adoption of digital health and increasing investments by market players to launch advanced connected self-care devices present lucrative opportunities in the market. Rising healthcare costs in developed countries is prompting patients to opt for self-monitoring of health vitals, facilitating the expansion of self-care medical devices across North America and Europe. Market drivers The Global Self-care Medical Devices Market Demand is driven by the rising prevalence of chronic diseases such as diabetes, hypertension, and cardiovascular diseases. According to WHO, cardiovascular diseases account for over 18 million deaths annually worldwide. Self-care medical devices enable timely monitoring and management of health vitals in chronic disease patients which otherwise require frequent hospital visits. This reduces healthcare costs significantly and improves access to quality care. PEST Analysis Political: Self-care medical devices market is regulated by government agencies for product approvals and reimbursements. Changes in regulatory policies can affect the sales and distribution of such devices. Economic: Volatility in economic conditions impact the disposable income of consumers and their spending on medical devices for self-care. Recession can lower the demand. Social: Growing health consciousness and aging population drive the adoption of devices for self-monitoring of chronic conditions. Lifestyle disease prevalence increases the focus on preventive healthcare. Technological: Advancements in digital connectivity and miniature designs facilitate online consultations and home usage of diagnostic tools. More user-friendly interfaces encourage self-management of treatment. Around 55% of the global market value is concentrated in North America due to the increasing incidence of chronic disorders and developed healthcare infrastructure in the United States and Canada. The self-care medical devices market is witnessing fastest growth in Asia Pacific on account of rising healthcare expenditure, growing epidemic of non-communicable diseases and expansion of private insurance coverage in China, India and other emerging nations. Get more insights on this topic: Self-care Medical Devices Marke  Rigid Knee Braces Market The rigid knee braces market caters to treatments of various knee injuries such as ligament tears, arthritis, sprains and damaged cartilage. Rigid knee braces provide stability and controlled motion to injured knees. Made of rigid thermoplastic or carbon fiber materials, they brace injured ligaments and joints by restricting movements. Some rigid knee braces have additional features like adjustable straps for customized fit and hinges to allow limited extension and flexion. Rising sports activities and work-related injuries have boosted the demand for rigid knee braces globally.

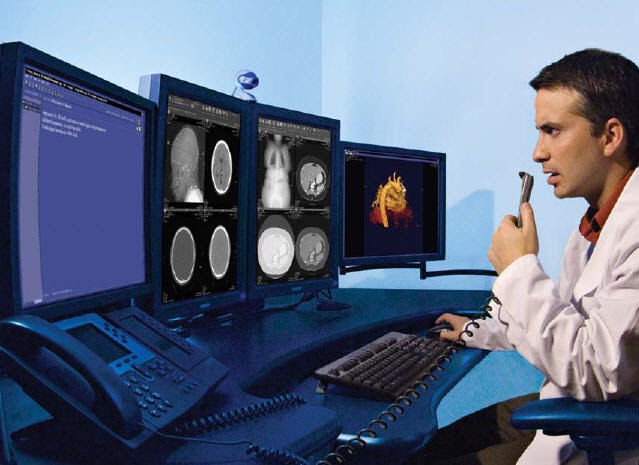

The Global Rigid Knee Braces Market is estimated to be valued at US$ 1142.1 million in 2024 and is expected to exhibit a CAGR of 6.6% over the forecast period from 2024 to 2030. Key Takeaways Key players operating in the rigid knee braces market are Mueller Sports Medicine, Inc., DJO Global, LLC, ACE Brand, Tynor Orthotics Private Limited, 3M Science, Mava Sports, Bauerfeind AG, Breg, Inc., Ossur, Thuasne USA, Zimmer Biomet, Kao Chen Enterprise Co., Ltd, Össur, Orthosys, Bauerfeind USA Inc., Orliman S.L.U., Steeper Inc., Beagle Orthopedic, Essity Medical Solutions, Bird & Cronin, LLC, Ottobock, Trulife, DeRoyal Industries, Inc., and Remington Medical Equipment. Major players are focused on product innovation and regional expansion to strengthen their market presence. Growing sports culture along with rising awareness about knee injury prevention through regular exercises and proper knee bracing present lucrative opportunities in the rigid knee braces market. Major companies are expanding their product portfolios with functionally advanced braces for various sports and activities to tap growth avenues. Key players are focusing on geographic expansion in emerging economies through extensive distribution networks and collaborations with local healthcare facilities. Increasing cases of knee injuries, awareness campaigns by associations and sports federations, along with government initiatives are encouraging adoption of rigid knee braces across global markets. Market Drivers Rising participation in sports and recreational activities has increased the risk of knee injuries dramatically. Long working hours in certain occupations that require prolonged standing or knee-heavy movements also contribute to injury risks. Growing prevalence of knee disorders like arthritis owing to obesity and aging population additionally propels the rigid knee braces market growth. Product innovation leading to development of lightweight and comfortable braces has boosted customer acceptance for rigid knee braces. PEST Analysis Political: The rigid knee braces market is regulated by various government organizations that ensure the quality and safety of medical devices. Regulations impact R&D investment and time to market for new products. Economic: Economic growth has increased discretionary spending on orthopedic devices. Rising healthcare budgets allow for more knee injury treatment and rehabilitation.However, inflation can increase production costs. Social: A growing health-conscious population is more aware of knee injuries from sports and daily activities. Also, an aging society needs more support for knee mobility and stability issues. This drives demand for customized braces. Technological: Advancements in materials like carbon fiber and 3D printing enable lightweight, discreet designs with precise fit. Sensor technology may allow for remote monitoring of healing progression. Data-driven innovation expands use cases. Geographical Regions of Concentrated Value North America accounts for the largest share of the global rigid knee braces market in terms of value, followed by Europe. This is attributed to factors such as the availability of advanced healthcare facilities, growing healthcare expenditure, rising incidence of knee injuries, presence of major market players, and favorable reimbursement policies in countries. Fastest Growing Geographical Region The Asia Pacific region is expected to grow at the fastest rate during the forecast period. This owes to rapidly improving medical technologies, increasing healthcare spending, large patient bases, and rising awareness about knee care. Population aging will further spike demand for supportive knee devices in China, India and other developing Asian markets. Get more insights on this topic: Rigid Knee Braces Market  PACS (Picture Archiving and Communication System) and RIS (Radiology Information System) are integrated software solutions that help to securely store, access, and exchange medical images and information across a hospital. PACS helps to securely store medical images that can be easily retrieved and assessed by radiologists and other clinicians from any connected device. RIS manages workflow, tracks radiology orders and results, and enhances productivity in radiology departments. The need for these systems is driven by the increasing adoption of digital imaging modalities such as MRI, CT scans, x-rays, and ultrasounds that generate a large volume of patient data daily.

The Global PACS and RIS Market Demand is estimated to be valued at US$ 4212.87 Mn in 2024 and is expected to exhibit a CAGR of 7.4% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the PACS and RIS market are 3A Composites GmbH, Multi-Pak USA, Inc., Laird Plastics, United Industries Group, Inc., Acrylitec Displays, Ray Chung Acrylic Enterprise Co., Ltd., Mitsubishi Chemical Corporation, Plaskolite, LLC, Lucite International, and Evonik Industries AG. 3A Composites GmbH is one of the leading providers of PACS and RIS solutions globally. The major factor driving the demand in the PACS and RIS market is the rising adoption of digital radiology modalities and growing need to digitally store and share increasing volumes of patient medical images and related data. According to a study, the United States conducted approximately 42 million MRI exams and 130 million CT scans in 2020. Technological advancements are also supporting the growth of this market. Vendors are focusing on integrating advanced features such as artificial intelligence, machine learning, and cloud computing into their PACS and RIS platforms. AI-powered solutions can automate routine diagnostic operations, enhance productivity, and support clinical decision making. Market Trends The cloud-based PACS and RIS solutions trend remains high in the market owing to advantages such as scalability, mobility, disaster recovery, and lower upfront costs. According to a third-party estimate, the cloud PACS market is projected to grow at 11% CAGR during 2023-2028. Increasing consolidation in the market is another key trend as major players pursue acquisitions to expand their customer base and product portfolios. For example, in 2022, Change Healthcare acquired Intelerad Medical Systems, a major provider of PACS and RIS solutions. Market Opportunities The growing medical tourism industry in developing nations presents significant opportunities for PACS and RIS vendors. These countries are actively investing in healthcare infrastructure development. Another key opportunity lies in offering comprehensive data analytics tools on top of the core PACS and RIS platforms. Aggregating and analyzing radiology data can generate actionable insights to optimize department workflows and improve treatment outcomes. Impact of COVID-19 on PACS and RIS Market Growth The COVID-19 pandemic has significantly impacted the growth of the PACS and RIS market globally. Due to the outbreak, majority of the hospitals and clinics experienced a dramatic increase in patient volume for imaging procedures like CT, MRI, ultrasound, etc. This exponential rise in imaging tests led to shortage of radiologists and burdened existing PACS and RIS systems with heavy data volumes. Many healthcare facilities struggled to efficiently store, exchange, retrieve and analyze such a massive amount of medical images and reports. This highlighted the immediate need to upgrade existing PACS and RIS infrastructure or implement new integrated systems with expanded storage capacity and faster data processing abilities. The demand for tele-radiology also surged as healthcare providers shifted to telemedicine and remote diagnosis to reduce physical contact amid social distancing restrictions. Vendors catering to PACS and RIS experienced a spike in their business during this period to help hospitals scale up their teleradiology capabilities. However, delayed elective surgeries and non-emergency care during peak pandemic times impacted the growth marginally. In the post-COVID era, the market is forecasted to grow steadily with continued investment in digitalization of radiology departments and long-term adaptation of hybrid virtual care models utilizing advanced medical imaging platforms like PACS and RIS. Geographical Regions with Highest PACS and RIS Market Concentration North America holds the largest share of the global PACS and RIS market in terms of value, attributed to factors like availability of advanced healthcare infrastructure, strict patient data management regulations and high adoption of digital technologies among medical facilities in the US and Canada. The Asia Pacific region is estimated to grow at the fastest rate during the forecast period. Countries like China, Japan and India are witnessing immense focus on modernizing their hospital radiology workflows with integrated PACS and RIS as part of large-scale healthcare reforms. Additionally, rapidly expanding medical tourism and private healthcare sectors and increasing healthcare expenditure in Asia Pacific economies are projected to drive the regional market growth of PACS and RIS. Fastest Growing Region for PACS and RIS Market The Asia Pacific region is poised to be the fastest growing market for PACS and RIS globally between 2024-2030. The growth can be ascribed to rising patient pool afflicted with diseases requiring diagnostic imaging, growing geriatric population, improving reimbursement scenarios, increasing investments by leading vendors and hospitals in medical infrastructure development, and expanding base of specialty radiology centers and private clinics. The presence of developing nations like India and China provides huge untapped market potential for PACS and RIS providers. Initiatives by governments in the Asia Pacific to reform public health systems and digitize medical records are also catalyzing the regional market expansion. With the rapid economic development and healthcare reforms, the Asia Pacific region is expected to stimulate significant demand for advanced PACS and RIS solutions during the forecast period. Get more insights on this topic: PACS and RIS Market  Vegan Food Market The vegan food market comprises plant-based food and beverages that do not contain meat, eggs, dairy, honey or any other animal-derived ingredients. Vegan foods such as plant-based meat, dairy alternatives, frozen desserts and ready-to-eat meals are becoming increasingly popular among health-conscious consumers. Many people adopt a vegan diet to avoid animal products for health, environmental or ethical reasons. The rising awareness about the negative impacts of meat consumption and benefits of plant-based nutrition is driving tremendous growth in the vegan food industry. The Global vegan food market is estimated to be valued at US$ 20721.19 Mn in 2024 and is expected to exhibit a CAGR of 12.% over the forecast period 2024 to 2030.

Key Takeaways Key players operating in the Global Vegan Food Market Growth are Abbott Laboratories, Biosynex, Qiagen Sciences LLC, Clinical Innovations LLC, Sera Prognostics, The Cooper Companies Inc., Medixbiochemica, Hologic Inc., IQ Products, NX Prenatal Inc., Promega Corporation, Medical Predictive Technologies Inc., Biosynex, Clinical Innovations LLC, NX Prenatal Inc., Medixbiochemica, Qiagen Sciences LLC, Sera Prognostics Inc., Insight Pharmaceuticals LLC, Creative Diagnostics. The growing popularity of flexitarian and vegetarian diets among millennials and Gen Z consumers is fueling significant growth in the plant-based food sector. Many new startups are innovating with vegan meat and dairy alternatives that offer similar taste, texture and cooking experience as animal products using plant-based ingredients. Market Trends The rise of blended families where vegan and omnivore diet preferences co-exist under one roof has led to increasing demand for multi-diet food packaging. Many brands are offering split packs that contain separate vegan and non-vegan options to make joint meal planning and grocery shopping more convenient. Another major trend is the development of meat-free jerkies, sausages and ready-to-eat sandwiches using vegan ingredients like soy, wheat and jackfruit that closely emulate meat texture. This allows vegan snacks and meals to seamlessly integrate into omnivore diets. Market Opportunities One major opportunity for vegan food companies is in caffeinated products like plant-based lattes, coffees and energy drinks. With increasing health consciousness spiraling into around-the-clock busy lifestyles, the need for convenient yet healthy caffeinated beverages has never been greater. Another key area of growth is vegan pet food made from ingredients suitable for both cats and dogs. As more pet owners adopt vegan diets themselves, they are looking for vegan kibble, treats and wet food for their furry companions as well. Impact of COVID-19 on Vegan Food Market Growth The COVID-19 pandemic has positively impacted the growth of the vegan food market. During the pandemic, health and wellness gained increased importance among consumers. People started preferring plant-based foods due to their associated health benefits. As vegan foods offer protein and other important nutrients from plant sources, their demand surged significantly. Online sales of vegan products also grew as more people purchased groceries through e-commerce channels. Companies witnessed increased interest in vegan foods as consumers sought sustainable and ethical options. New product innovation and launches in vegan categories like meat and dairy alternatives ensured availability. The pandemic heightened awareness about veganism and its relationship with immunity and gastrointestinal health. This boosted trial and uptake of vegan diets. Post pandemic, the health-conscious consumer base interested in veganism is expected to retain, propelling further market growth. However, disruptions to supply chains and price rises of key crops in the initial period impacted production and availability. The market value concentration of the Vegan Food Market was highest in North America pre-COVID driven by growing vegan population. The region continues to be a major hub of vegan companies and food innovations. Awareness about veganism, health issues and environmental sustainability are primary drivers of its fast growth. Countries like the US and Canada are recognized for having the maximum number of vegans and vegan product launches annually. Asia Pacific is the fastest growing regional market fueled by rising health consciousness of its population and animal welfare concerns. The increasing presence of international vegan brands is making alternative options widely available in the region. Get more insights on this topic: Vegan Food Market Explore More Articles: India Power Tool Market  The thermal printing market has witnessed significant growth over the past few years owing to its advantages of being portable and compact. Thermal printing technology is used for various applications including POS/billing, labels and tickets, security surveillance, logistics and transportation. Thermal printing provides instant, invisible barcode and text printing on heat-sensitive paper or receipts without using ribbons or toners. With no ink cartridges or rollers required for printing, it offers durable, high-quality and cost-effective printing solutions. Growing adoption of thermal printers in industries such as healthcare, retail, logistics and transportation is further expected to drive the thermal printing market.

The Global Thermal Printing Market Demand is estimated to be valued at US$ 54.31 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2030. Key Takeaways - Key players operating in the thermal printing market are PharmaZell, ABIL CHEMPHARMA PRIVATE LIMITED, ICE, Grindeks, Suzhou Tianlu Bio-pharmaceutical Co.,Ltd, ARCELOR CHEMICALS PRIVATE LIMITED, Dipharma Francis S.r.l. These players are focusing on new product launches and partnerships to strengthen their market position. - The thermal printing market is witnessing significant demand from the healthcare sector. Various applications such as medical labels, medical reports and drug tracking are spurring the use of thermal printers in hospitals and pharmacies. - Technological innovations are helping improve the functionality of thermal printers. Newer technologies allow integration of thermal printing into IoT and Industry 4.0 applications. Advanced features such as wireless connectivity, barcode reading and analytics capabilities are further enhancing the demand. Market Trends -Mobile thermal printing is emerging as a key trend with increasing focus on portable printing solutions for field sales, delivery and transportation applications. More compact and long battery life printers are being developed. -Thermal transfer over direct thermal printing is gaining popularity due to its ability to print on various types of substrates including rough surfaces, coloured backgrounds and synthetic materials. Market Opportunities -Growing applications of blockchain for supply chain management are opening new opportunities for integrating thermal printers. Blockchain-enabled printers can help trace shipments and monitor quality in real-time. -Adoption in new verticals such as construction, energy and utilities provides significant headroom for growth. Thermal printing solutions catering to jobsite labelling, asset tagging and work management in these industries can drive the next phase of expansion. Impact of COVID-19 on Thermal Printing Market The COVID-19 pandemic has significantly impacted the growth of thermal printing market. During the initial phase of lockdowns, the demand from retail and healthcare sectors declined sharply as most of the establishments were closed. This led to a fall in shipments of thermal printing consumables like thermal paper and ribbons. However, as the pandemic intensified, there was a rise in demand from healthcare and pharma packaging applications. Thermal printing found widespread use in printing medical prescriptions, labels for medicine packaging and temperature verification labels for vaccine transportations. E-commerce sector also witnessed a surge in demand which drove the uptake of thermal printing solutions for labeling parcels and packages. Post pandemic, the demand from retail and hospitality industries is recovering gradually as businesses resume operations with safety protocols. Meanwhile, the demand from healthcare and pharma industries is anticipated to remain high. Adoption of contactless transactions and QR code payments has increased significantly which is boosting the demand for portable thermal printers. With social distancing becoming a new normal, thermal printing will play a crucial role in various applications like event ticketing, boarding passes, printing digital menus at restaurants. Manufacturers are focusing on developing advanced technologies like auto-cut printers and integrated barcode scanners to facilitate contactless transactions. Overall, while COVID-19 posed short term challenges, it has opened new growth opportunities for thermal printing market. Geographical Regions With Highest Thermal Printing Market Value North America represents the largest market for thermal printing solutions in terms of value, accounting for over 35% share of the global market revenue. Presence of major industry players, well established distribution networks and early adoption of advanced technologies drives the thermal printing market growth in the region. Europe is the second largest regional market supported by wide usage of thermal printing solutions across various industries in countries like Germany, UK and France. Asia Pacific market is expected to witness the fastest growth during the forecast period due to rising demand from emerging economies like China, India and South East Asian nations. E-commerce boom, increasing digitization of processes and expanding manufacturing sector will augment the demand for thermal printing in Asia Pacific region. Fastest Growing Regional Market for Thermal Printing Asia Pacific region is poised to be the fastest growing regional market for thermal printing during the forecast period. This is attributed to evolving demographic dynamics, rising disposable incomes, increasing penetration of digital technologies and growing industrialization in Asia Pacific countries. China represents the largest thermal printing market in Asia Pacific region, followed by India and other Southeast Asian nations. Proactive government initiatives to foster digital transformation, supporting local manufacturing and promoting cashless economies will propel the demand for versatile thermal printing solutions across multiple end-use industries. Furthermore, expansion of global companies into Asia Pacific coupled with emergence of local manufacturers offering cost-effective thermal printing products are driving comprehensive market growth in the region. Get more insights on this topic: Thermal Printing Market Explore More Articles: India Coronary Stents Market  https://www.coherentmarketinsights.com/market-insight/plasma-expander-market-5939 Plasma expanders, also known as blood volume substitutes or volume expanders, are solutions used to expand blood plasma volume during surgery or trauma care. They work by increasing the amount of fluid present in the blood vessels and exerting an oncotic pressure effect that helps bring fluid back into the intravascular space from the extravascular space. Common plasma expanders include hydroxyethyl starch, gelatin, human albumin, and dextran. Plasma expanders are vital for surgical procedures involving substantial blood loss to replace lost plasma oncotic pressure and intravascular volume. The rising geriatric population undergoing various surgical interventions and the increasing incidence of trauma cases due to road accidents are key factors driving the demand for plasma expanders. The Global Plasma Expander Market is estimated to be valued at US$ 32.58 Mn in 2024 and is expected to exhibit a CAGR of 8.0% over the forecast period 2024 to 2030.

Key Takeaways Key players operating in the Global Plasma Expander Market Share are Asahi Kasei Pharma Corporation, Weldon Biotech Inc., Abbexa Ltd., Laboratory Corporation of America, Biocompare, EFK Diagnostics, Elabscience Biotechnology Inc., Abbot, Diazyme Laboratories Inc., Abnova Corporation, BSBE, Maccura Biotechnology Co.,Ltd., LifeSpan BioSciences Inc., Biomatik, Geno Technology Inc., AMS Biotechnology (Europe) Limited, Epinex Diagnostics Inc., and DxGen Corp. The rising volume of surgical procedures performed worldwide and trauma cases are fueling the demand for plasma expanders. Various types of plasma expanders including hydroxyethyl starch, gelatin, human albumin, and dextran are being increasingly utilized during surgical interventions and for trauma care. Technological advancements are aiding in the development of newer plasma expander formulations with enhanced safety profiles and oncotic pressure sustaining capabilities. Market Trends Some key trends being observed in the plasma expander market include growing demand for synthetic varieties of plasma expanders. Synthetic plasma expanders have certain advantages over albumin varieties such as greater availability and lower risks of disease transmission. Rising focus on development of non-gelatin based plasma expanders. Traditionally, gelatin was widely used as a plasma expander. However, non-gelatin varieties are now gaining popularity due to certain religious concerns related to the use of gelatin. Market Opportunities The plasma expander market players have strong opportunities for growth in emerging economies due to rapid development of healthcare infrastructure and rising purchasing power. Growing adoption of minimally invasive and advanced surgical techniques will further propel utilization of plasma expanders. There is scope for innovations leading to development of newer generations of plasma expanders with longer duration of action, lower risks, and enhanced benefits compared to existing products. Impact of COVID-19 on Plasma Expander Market The COVID-19 pandemic has significantly impacted the growth of the plasma expander market. The increasing prevalence of various chronic diseases and growing number of trauma cases worldwide were driving the market growth pre-COVID. However, due to the outbreak of COVID-19, many countries imposed strict lockdowns and travel restrictions. This led to delayed or canceled elective surgeries and non-emergency medical procedures to avoid unnecessary exposure and focus healthcare resources on treating COVID-19 patients. As a result, the demand for plasma expanders from surgical centers and hospitals reduced substantially during the peak of the pandemic. Post-COVID, as lockdowns are being lifted and healthcare services resume, the demand for plasma expanders is recovering gradually. However, it may take some time for the market to reach pre-COVID levels. Manufacturers are facing challenges in terms of disrupted supply chains and shortage of raw materials. At the same time, there is increased focus on developing more effective plasma expanders to treat critically ill COVID-19 patients suffering from conditions like shock, acute respiratory distress syndrome (ARDS), etc. Going forward, the market is expected to witness steady growth driven by factors like the rise in surgical volumes, trauma cases, and chronic disease burden globally. However, the impact of recurring COVID waves continues to add uncertainty. Geographically, North America dominates the plasma expander market in terms of value, owing to the high healthcare spending and presence of major players in the region. Europe is another prominent regional market driven by the rising prevalence of lifestyle diseases, aging population, and technological advancements. On the other hand, Asia Pacific is projected to be the fastest-growing region during the forecast period due to increasing medical tourism, healthcare infrastructure development, and growing disposable incomes in developing countries like China and India. Get more insights on this topic: Plasma Expander Market Explore More Articles: Hydro Turbine Generator Unit Perilla Extract Market Will Grow at Highest Pace Owing to Expanding Healthcare Applications2/27/2024  The perilla extract market has gained extensive traction due high demands from health-conscious consumers for natural remedies. Perilla extract oil is derived from perilla seeds contains high amount of alpha-linolenic acid (ALA), which is an omega-3 fatty acid. It provides various health benefits such as reducing inflammation, improving brain and heart functions. The oil also possess disease preventing properties against diabetes, asthma, and cancer. Due to expanding applications in healthcare, pharmaceutical, and food and beverage industries, the global perilla extract market is estimated to be valued at US$ 1.33 Bn in 2024 and is expected to exhibit a CAGR of 15.% over the forecast period 2024 to 2030.

Key Takeaways Key players operating in the perilla extract market are Thales Group, Alstom, Huawei, Hitachi, Siemens, Cisco Systems, IBM, Microsoft, and Intel. These manufacturers are focusing on adopting innovative extraction techniques like supercritical fluid extraction to obtain high-quality perilla extracts. The demand for perilla extract is growing rapidly from the pharmaceutical sector owing to numerous medicinal uses. The extract has shown effective results in preventing multiple health conditions like asthma, diabetes, and cancer. It is also known for relieving anxiety and improving cognition. Technological advancements like development of advanced extraction methods using supercritical CO2 are helping manufacturers to obtain standardized, pure perilla extract oils with high omega-3 content. Supercritical fluid extraction is a green technology that allows for selective separation of compounds from perilla seeds. Market Trends Increased focus on R&D of perilla extract products - Manufacturers are investing extensively in development of standardized perilla extract ingredients and products with customized formulations for various application industries. Novel delivery formats like perilla infused beverages and dietary supplements are gaining popularity. Growing demand for clean label and natural ingredients - With rising health awareness, consumers prefer food and beverages with simple and recognizable ingredients sourced from natural plants. Global Perilla Extract Market Demand meets these clean label demands owing to its natural source. Market Opportunities Utilization in cosmeceuticals - Perilla extract possesses high antioxidant and anti-inflammatory compounds that can be leveraged for developing natural skin care products. Its potential in anti-aging creams and serums remains untapped. Formulating functional foods - Perilla extract can be incorporated in developing foods for specific health benefits like omega-3 enrichment. Products like perilla infused snacks, dairy and beverages present lucrative opportunities. Impact of Covid-19 on Perilla Extract Market Growth The COVID-19 pandemic has significantly impacted the growth of the perilla extract market globally. During the initial phase of the pandemic, lockdowns imposed worldwide halted production and supply chain activities. This led to disruptions in the availability of perilla extract. With people confined indoors, the demand for health and wellness products also took a hit initially. However, as the pandemic prolonged, awareness regarding health and immunity boosting grew exponentially. This increased the consumption of perilla extract globally as it is known to have antioxidant and anti-inflammatory properties that boost the immune system. As restrictions eased in 2021, manufacturers resumed operations with requisite safety measures and protocols in place. This helped stabilize the supply situation. The market is expected to witness steady growth post-pandemic as consumers have now realized the importance of bolstering health to mitigate viral attacks. Also, ongoing research for potential benefits of perilla extract in fighting viral infections is anticipated to further boost demand. Companies are focusing on expanding production capacities and enhancing distribution networks to cater to rising requirements in the coming years. Geographical Regions With Highest Perilla Extract Market Value Currently, the Asia Pacific region accounts for the largest share of the global perilla extract market in terms of value. This is majorly attributed to high consumption of perilla extract products in countries such as Japan, China and South Korea where it is a popular culinary and medicinal herb. Easy availability along with lengthy usage of perilla in traditional medicines and cuisine has made APAC the dominant market. North America follows APAC in market size due to increasing popularity of perilla extract among health-conscious consumers and its usage in supplements, beverages and packaged food products. Availability of import substitutes and indigenous production is driving the market growth in countries like the US and Canada. Progressive lifestyles and growing awareness about nutritional benefits are prompting consumers in Europe to include perilla extract in their diets as well, making European market an important region. Fastest Growing Regional Market for Perilla Extract The Middle East and Africa region is expected to witness the fastest market growth for perilla extract during the forecast period. This growth can be primarily attributed to rising health consciousness among consumers regarding immunity boosting supplements and herbs. Emerging economies across Africa are showing high potential backed by growing disposable incomes, urbanization and changing food habits. Market players are investing in establishing production facilities and promoting various applications of perilla extract including its anti-inflammatory properties that help arthritis patients and skin benefits. Favorable climatic conditions allow for cultivation of perilla in many African countries as well which can augment regional supply. As awareness rises, the MEA region is poised to emerge as a key market for perilla extract globally over the next years. Get more insights on this topic: Perilla Extract Market Explore More Articles: Cocktails Syrups |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2024

Categories

All

|

RSS Feed

RSS Feed